On surface level, Intel (NASDAQ: INTC) appears to be a risky trade. For one thing, INTC stock has struggled conspicuously in recent sessions, down more than 10% in the trailing five days and losing 12% in the past month. It also doesn’t help matters that IBM (NYSE: IBM) suffered a catastrophic drop due to rough preliminary earnings figures.

Table of Contents

Nevertheless, from a technical perspective, contrarian traders have reason to hope. After all, INTC stock is up over 179% on a year-to-date basis. Generally, you don’t see that kind of sustained performance unless there’s true substance behind the rally. Of course, that’s all past data — data that has surely been integrated into the share price. So, what could get the needle moving forward this time?

Naturally, market participants are looking to Intel’s upcoming second-quarter earnings report, scheduled for release on July 23. Analysts will be looking for earnings per share of 19 cents on revenue of $14.4 billion. In the most recent quarter, Intel reported EPS of 29 cents, beating the consensus view of a loss of 1 cent. Revenue came in at $13.58 billion, exceeding the estimate of $12.4 billion.

It must be said that nobody knows what may happen when the tech giant discloses its financials. What makes earnings season so dangerous is that, even with positive results, it’s not 100% guaranteed that INTC stock will move per bullish investors’ wishes. Still, for what it’s worth, the prediction market seems optimistic.

According to a 24/7 WallSt report, “Polymarket contracts tied to the July 23 release put a 68.5% probability on Q2 Foundry revenue exceeding $5.5B and a 75.5% probability on Data Center & AI clearing $5B. Guidance from management already calls for revenue between $13.8B and $14.8B. The full-chain put/call ratio sits at 0.30, a decisive skew toward calls, and insider activity across 47 recent transactions is net buying.”

Frankly, I would be careful about over-interpreting the low put/call ratio as this metric is just a tally of volume and tells us nothing about transaction initiation. Setting that aside, the popular consensus does seem to point to Intel potentially delivering the goods, which could boost INTC stock.

Balance of Order Flow May Favor a Near-Term Trade for INTC Stock

Interestingly, at the same time people are placing their hopes on Intel stock enjoying a post-earnings pop, INTC itself has been stuck in a bearish cycle. Over the past 10 weeks, only three weekly candlesticks were positive, thus leading to an overall downward slope.

For those that believe ‘the trend is your friend until it ends,’ INTC stock is at great risk of continuing its descent. Being that there are questions about artificial intelligence — specifically the expense associated with the industry and the sustainability of the overall business — it wouldn’t be shocking to see extended bearishness.

However, another argument exists, one revolving around mean reversion. When a security has been beaten up over some length of time, it’s likely that a significant volume of the weak hands has been flushed out. Further, more negative news will be needed to justify continued pessimism. As such, a contrarian catalyst may have a disproportionately positive impact on trading sentiment.

Fundamentally, modern equity markets are dominated by algorithmic, rules-based trading. Indeed, I would argue that they have to be. Think about the logistical reality of the contemporary environment. At the very moment that critical information is released to the public, it’s instantly digested by trading bots and machines. In this elite world, if you blink an eye, you’re too late.

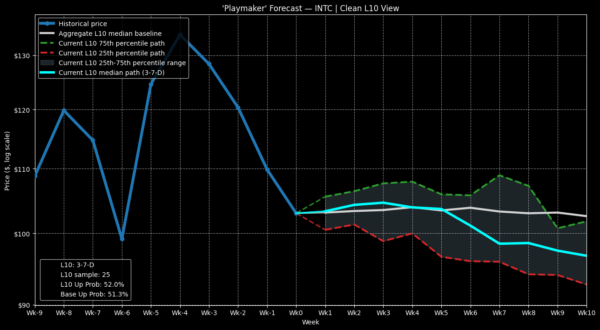

Basically, I’m counting on these algorithms to perceive INTC stock as a temporary discount. With seven down weeks printed, the algos likely smell blood in the water. If we look at past empirical data, it would seem that a negative balance of order flow influences how future outcomes pan out.

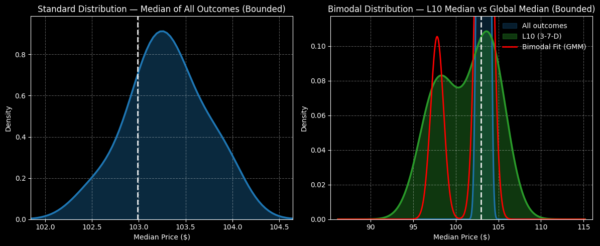

Conditioned for the 3-7-D sequence — which has flashed 25 times since January 2019 — the expected forward 10-week median distribution lands between $90 and $110 (assuming a starting price of $102.99). Further, peak probability density is expected to print at $104.70, suggesting a modest upward bias.

Compare that to the random baseline, where buying INTC stock by chance at the same starting price above would likely yield a thinner 10-week distribution between $102 and $104.50. Probability density in this case would likely land at $103.25.

Targeting a Specific Bull Spread

Am I suggesting that an average positive variance of 1.21% is that much to write home about? No and if I’m being honest, it’s risky to trade Intel stock — as choppy as it can be — based on this modest advantage. However, the enhanced performance of the 3-7-D signal isn’t orderly and linear relative to the baseline.

Taking a closer, inductive look at the data, week 3 following the flashing of the aforementioned signal represents the typical peak outcome value before INTC stock historically falls off. If we were to look strictly at the numbers, we would expect Intel to hit $105. Subsequently, a logical idea to consider is the 103/105 bull call spread expiring July 31.

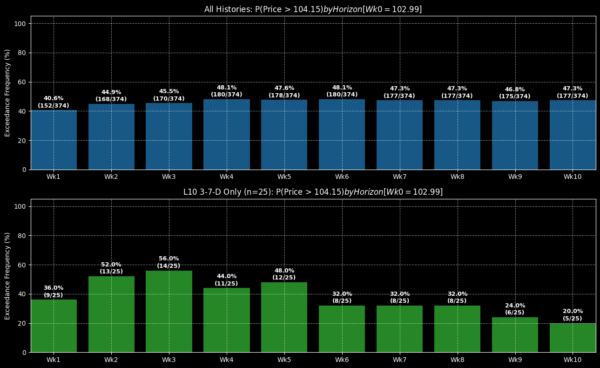

Should Intel stock rise through the $105 strike at expiration, traders would secure a payout of nearly 74%. While it’s not the greatest reward, the net debit required is only $115. But what’s perhaps most fascinating is the breakeven price of $104.15.

Right now, the market is assigning a probability of profit (the odds that INTC stock will reach break even) at 48%. This figure is calculated as a function of implied volatility within the Black-Scholes framework, which assumes a risk-neutral, log-normal paradigm. In other words, it’s a theoretical probability.

I’m disputing these odds. Of the 25 times that the 3-7-D signal has flashed, we have seen INTC stock rise through the equivalent price of $104.15 a total of 14 times in week 3. That means the “real” probability of profit could be 56%, some eight percentage points higher.

Now, I want to be clear that neither I nor the Black-Scholes model has an exclusive hold on the truth. However, in my defense, I’m relying on a what-you-see-is-what-you-get framework of calculating odds of success. Black-Scholes, on the other hand, uses a complex, opaque calculation to come up with its projection.

Ultimately, it’s up to you to decide which model you believe best represents reality. But based on past historical outcomes, there’s a reasonable case to be made that this Intel stock options spread is favorably mispriced.

Leave a Reply