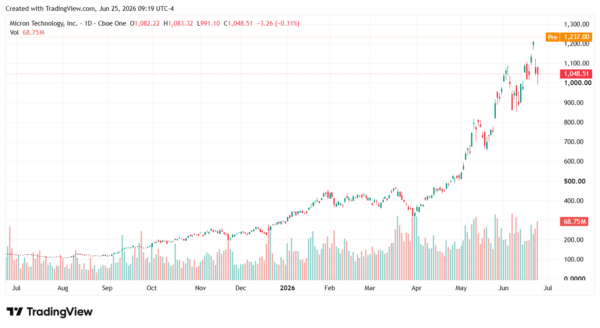

Micron Technology (NASDAQ: MU) is exploding higher after the memory-chip giant delivered another blockbuster earnings report, fueled by unprecedented demand for artificial intelligence infrastructure, which shows no clear signs of cooling off.

Table of Contents

In addition, with AI data centers consuming massive amounts of high-bandwidth memory (HBM), MU has become one of the biggest beneficiaries of the boom, posting revenue and profit growth that far exceeded Wall Street expectations.

However, while investors are cheering results and bullish guidance, history suggests caution.

Let’s start out with the good news.

Micron’s AI-Fueled Growth Is Accelerating

Micron’s adjusted EPS of $25.11 was well above estimates of $20.78. Revenue of $41.46 billion was also well above estimates of $35.84 billion. Revenue was also well above the $9.3 billion posted year over year. For the current quarter, MU expects to see revenue of about $50 billion, which would be another massive year over year jump from $11.3 billion.

In addition, as noted by CNBC, “While all four of Micron’s business units saw revenue multiply, the most explosive growth was in the core data center business, where sales climbed more than sevenfold to $11.5 billion from $1.53 billion in the same period a year ago. In addition to memory, Micron also recorded over $5 billion in data center solid state drive revenue.”

That explosive growth explains why shares of MU surged about 15% in after-hours trading. From here, as long as demand for memory chips continues to outpace available supply, MU could have room to push even higher.

Why Investors Shouldn’t Ignore Industry Risks

Fueled by surging demand for AI infrastructure, data centers, and high-bandwidth memory solutions, MU has emerged as one of the semiconductor industry’s biggest winners. The company’s advanced DRAM and NAND memory products have become critical components in AI servers, helping drive significant revenue growth and investor enthusiasm.

But the good times could come to an end once production increases, especially as Samsung and SK Hynix build new fabrication plants to boost production capacity. When that happens, and when supply again overtakes demand, stocks like Micron could easily reverse lower. History is also proof investors should be cautious. Between 2022 and 2023, the memory crash led to MU reporting a GAAP net loss of $2.31 billion in just one quarter, as noted by Trefis.

“During 2018 and 2019, cloud operators over-ordered memory through 2017, then steadily reduced purchases through 2018 as inventories swelled. NAND prices fell roughly 60% and DRAM approximately 40%. Micron peaked near $64 in May 2018 and fell to around $28 by year-end,” they added.

Where Micron Goes From Here

Micron is one of the biggest winners of the AI infrastructure boom.

Demand for advanced memory solutions continues to accelerate as hyper scalers, cloud providers, and AI developers race to expand computing capacity. All of which could support further gains in MU stock, especially if supply remains constrained and pricing stays strong.

However, today’s shortages and soaring prices could eventually give way to oversupply and falling margins as competitors ramp production. While Micron’s latest earnings report reinforces the strength of what’s happening, long-term investors should keep a close eye on industry capacity. Once that improves, Micron could start to fall apart.

Leave a Reply