Jerome Powell keeps saying inflation is headed to 2%. Kevin Warsh backs him up, talking up the Fed’s commitment to price stability like it’s a settled question. The bond market isn’t buying a word of it because unlike the talking heads on a panel, bond investors put actual money behind their disagreement.

Table of Contents

Why would they?

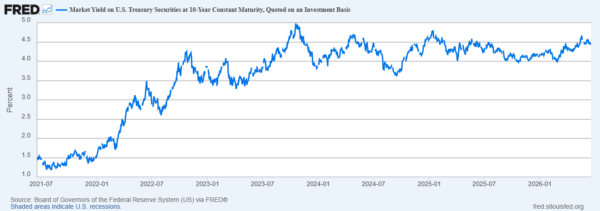

The yield on the 10-Year Treasury recently pushed above 4.5%. The 30-Year cleared 5%. Those yields are the foundation everything else in finance gets priced off of – your mortgage, your company’s borrowing costs, the multiple Wall Street is willing to slap on every growth stock you own.

But you see, a market that genuinely believed inflation was heading to 2% with rate cuts coming wouldn’t be demanding some of the highest long-term yields we’ve seen in years. Which tells you that the bond market is calling the Fed’s bluff in real time, with trillions of dollars behind the bet.

Bond Investors Are Underwriting The Next Three Decades.

The Fed’s job is narrow –inflation, employment, financial stability, measured in quarters. A pension fund buying a 30-year Treasury isn’t playing that game. They’re underwriting purchasing power three decades out, government borrowing across multiple administrations and multiple crises nobody’s predicted yet, and whether the dollars they get back will still mean anything when they get them.

That’s a completely different bet than guessing next month’s CPI print.

Chicago Fed President Austan Goolsbee already acknowledged inflation has moved the wrong direction, and the last stretch back to target is proving harder than the easy progress it made. The bond market priced that risk in before Goolsbee said it out loud. Inflation has cooled a lot from the 2022 peak. Yet yields haven’t followed it down because investors are trying to determine what inflation looks like over the next 3 decades, not the next quarter.

Washington’s Borrowing Habit

Inflation gets the headlines because it’s easy to talk about on TV. Debt is the bigger problem, and it’s getting almost no airtime relative to its size. We’re carrying north of $36 trillion in federal debt now, with interest expense becoming one of the fastest-growing costs in the entire federal budget… faster-growing than most line items anyone in Washington actually wants to discuss in an election year.

Run the logic forward. Deficits don’t close themselves. The Treasury has to issue more debt to cover them. More issuance means more supply hitting the market. More supply means buyers get to demand a better price for showing up – and that price is yield. The Treasury market is the deepest, most liquid market on earth, and it still answers to the same supply-and-demand math as everything else. You can’t flood a market with trillions in new paper every year and expect buyers to keep accepting the same terms forever.

That’s what’s actually being priced into the long end right now. Not just where inflation lands next year, whether the U.S. can keep borrowing at this scale without eventually having to pay up for the privilege.

If You’re Trading Equities And Ignoring This, You’re Trading Half-Blind

Most traders live inside earnings prints and chart patterns and treat the bond market like it’s somebody else’s problem. That’s a mistake that gets expensive fast, because Treasury yields set the terms everyone else is playing under whether they realize it or not. Higher yields mean a higher discount rate on every future cash flow, which hits growth names hardest, since their value sits furthest out on the timeline. Private equity financing gets pricier. Commercial real estate eats another round of pressure. Corporate borrowing costs climb across every sector simultaneously.

None of that stays contained to a bond desk. It bleeds into equities with a lag long enough that most traders don’t connect the dots until their own positions are already bleeding too. The real question isn’t whether the Fed cuts once or three times this year. It’s whether rates are settling into a structurally higher range than almost anybody priced in twelve months ago – and that single shift reaches into tech valuations, housing, and credit markets in ways that dwarf whatever happens at the next FOMC meeting.

We’ve Run This Playbook Before

History doesn’t repeat exactly, but it rhymes enough to matter. Through the late ‘60s and most of the ‘70s, policymakers kept telling markets inflation pressure would fade on its own. Bond investors didn’t buy it then either, and they kept demanding higher yields to compensate for risk they didn’t believe was actually handled. Inflation eventually proved them right.

Although today’s setup isn’t identical – stronger economy, more credible Fed, deeper markets – the mechanism hasn’t changed an inch. Bond investors still care about whether the money they get back is still worth something. When that confidence cracks, yields go up and it doesn’t matter how convincingly the people in charge insist otherwise.

Pay Attention Now

Stocks like NVIDIA (NASDAQ: NVDA) dominate the news cycle because they move fast and make for good headlines. On the flip side, bonds move slowly, then all at once, and by the time everyone notices, the damage is already done. A rising 10-Year works its way into your mortgage, your company’s capital plans, your retirement account, and the multiple Wall Street pays for your stocks, whether you’re watching for it or not.

Maybe inflation keeps cooling. Maybe Washington gets its deficit under control. Maybe the market just absorbs the issuance without blinking. None of that is priced in right now. And that gap, between the comfortable story the Fed keeps telling and the price bond investors are actually demanding, is one of the more important disagreements in markets today. When trillions of dollars start pricing a different future than the one policymakers keep selling, everyone should pay attention.

Leave a Reply