There’s really no other way to characterize the market performance of electric-vehicle manufacturer Lucid Group (NASDAQ: LCID) other than absolutely disastrous. Since the start of the year, LCID stock is down about 45%. That alone is enough to make retail traders run for the hills. Nevertheless, it’s clear that the smart money senses the very real possibility of upside — serious, blistering upside.

Table of Contents

Now, for the million-dollar question: how in the world does that make any sense? It doesn’t until you look at the quantitative data.

First, let’s go over the fundamental reasons why LCID stock has performed so poorly — and why some traders might view Lucid as so bad, it’s good. Obviously, it’s impossible to ignore the EV manufacturer’s horrific financial disclosure for the first quarter, where it suffered its biggest revenue miss in more than four years. Also, the suspension of full-year guidance was icing on the bear cake.

Pouring salt on open wounds were production problems with the Gravity SUV. While the underlying issue was reportedly solved, the matter further represented an example of Lucid struggling to scale manufacturing efficiently. As well, you have the chokepoints of persistent losses and ugly margins. Basically, there hasn’t been a whole lot to be excited about when it comes to LCID stock.

And yet, Lucid isn’t without merits. Some of the most speculative traders appear to be focused on Uber Technologies (NYSE: UBER) expanding its partnership with the EV maker. Moreover, Saudi Arabia continues to provide significant financial support. In addition, production of Gravity continues to move forward despite the hiccups.

Sure, the equity market is clearly focused on the losses, production issues and the guidance withdrawal. However, call buyers (the options speculators) appear to be equally focused on the positives. Because so much bad news is baked into LCID stock, it arguably wouldn’t take much to spark a turnaround, no matter how brief.

Plus, with the calls being nominally cheap, there’s almost a nihilistic attitude toward Lucid stock. Yes, there’s risk — but the upside potential is gargantuan.

Volatility Skew Reveals How the Smart Money is Approaching LCID Stock

One of the best pieces of evidence regarding the above assertion comes from the volatility skew. By definition, the skew represents implied volatility (IV) across the strike price spectrum of a given options chain. Since IV reflects the pricing potential of the selected strike, sophisticated traders attempt to cover the underlying implied move.

Think of the volatility skew as an insurance market. On any given day, a popular security is likely going to move up or it’s going to move down. Options traders, especially the pros that are handling massive funds, must decide which trajectory is more likely — and subsequently hedge against that risk.

Typically, a skew will feature put dominance on the left-side tail, thus providing insurance against downside movements. However, call dominance tends to be the order of the day on the right side, which allows traders to lever up rallies. In this manner, sophisticated players make sure they’re not caught out, either with a sudden correction or a blistering blowoff.

However, the skew for Lucid stock (for the June 26 expiration date) is rather unique. As expected, put dominance exists on the left-side tail, implying a prioritization of risk mitigation. With LCID stock losing about 78% over the past 52 weeks, that’s a smart play — I’d go so far as to say it’s the only play.

But the revealing part comes from the right side. As the strike price rises, call dominance becomes more prominent. Essentially, the skew for LCID stock is convexity-oriented. Yes, it’s obvious that traders don’t want to be caught with their pants down if Lucid tumbles. Yet they also don’t want to be walked in on if shares skyrocket.

And that’s the vexing problem with Lucid stock. I call it a two-true outcome trade — either it’s going to strike out or it’s a homerun.

Triangulation Reveals an Intriguing Narrative

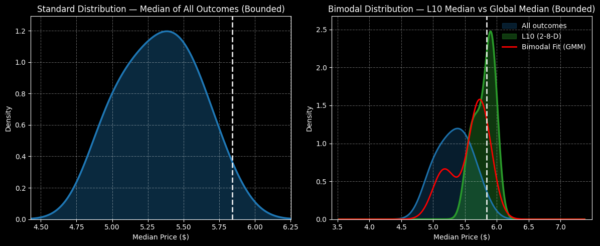

If you were to buy and hold LCID stock for a 10-week period, the chances of the position being profitable are extremely limited. We’re talking about an exceedance ratio — whether the stock rises above the starting point — of 27.8%. Nominally, the forward distribution is awful. Assuming a starting price of $5.84, you’re looking at LCID landing between roughly a median price of $4.50 and $6.25.

The saving grace here is the current quantitative sequence. In the past 10 weeks, Lucid stock printed only two up weeks, thereby leading to a downward slope across the period. Under this 2-8-D signal, the 10-week forward distribution shifts positively, potentially landing between $5.30 and $6.30. Notably, the exceedance ratio pops to 60%.

Now, is that enough justification to buy LCID stock? I would hesitate to rely purely on the inductive model above because of the two-true outcome situation. Here, using median pricing calculations is deceptive because Lucid is likely to jump to extreme highs or fall to extreme lows. When you take the median of these extremes, you get the middle value — but this value is really an artifact.

With such robust mobility in LCID stock, you’re not likely to come across the middle value. So, why are sophisticated traders buying far out-the-money (OTM) calls? It probably just comes down to the obvious point: they’re cheap.

Let’s say you bought the 7.00/8.00 bull call spread expiring June 26. If LCID stock rises through the $8 strike at expiration, you earn a maximum payout of roughly 456%. The net debit for this spread is only $18. History has proven that $8 is reachable given how much Lucid moves.

Unfortunately, the opposite is also true: LCID stock is just as liable to falter and land flat on its face. So, what’s interesting here is that the smart money — even when acknowledging the risks — is willing to take the shot.

Ultimately, if you have some stupid money lying around, you could consider a what-the-heck trade. But anything other than that is a ridiculous gamble.

Leave a Reply