In Japan right now, an increasing number of residents have been struggling with a literal bear invasion. And I’m afraid this metaphorical scenario continues to plague PayPal (NASDAQ: PYPL) investors. With society increasingly embracing digital transactions, you’d think that PYPL stock would enjoy relevance. However, that golden age may be over.

Table of Contents

This isn’t to say that PYPL stock has lost its fundamental relevance. Far from it, the underlying business model and various technologies have become standard fare in the modern economy. Unfortunately, PayPal has been rapidly shedding its distinguishing value, with multiple competitors eating up market share in key sectors. To be blunt, the brand is just another label among several.

Primarily, the biggest concern impacting PYPL stock is arguably branded checkout growth, which has weakened materially. This segment is the higher-margin, higher-quality part of PayPal’s business — the classic “Pay with PayPal” button. Growth here has decelerated to around 1% to 2%, which investors interpret as a major red flag.

As mentioned earlier, compounding the woes affecting PYPL stock is the intensified competition. Principally, Apple’s (NASDAQ: AAPL) Pay and Wallet, Stripe, and Klarna (NYSE: KLAR) are squeezing PayPal’s margin. It should be noted that KLAR stock isn’t exactly a top performer, as the fintech specialist has suffered a roughly 48% year-to-date loss.

However, that’s the issue with this payments arena — there’s just no real differentiation. Sure, individual fintechs will wax poetic about their unique value proposition, but let’s be real. For consumers, you tap your phone, push a button, send money and enjoy BNPL (buy now, pay later) financing. Most major platforms (including some native checkout systems from major merchants) broadly do the same thing.

In other words, there’s really no compelling reason to use PayPal (or any other platform) exclusively. Plus, switching among various platforms is a seamless process incentivized through various enticing benefits and programs. Again, PYPL stock is just another solution among several.

Volatility Skew Confirms Hesitation for PYPL Stock

Of course, none of the information cited above is groundbreaking. Since PayPal stock is down 24% YTD, we can reasonably presume that the bad news has been baked into the share price. The big question is whether or not too much pessimism is weighing down PYPL. If it is, a bit of good news could create a disproportionately positive impact.

That’s the basic technical premise behind a contrarian position in PYPL stock, and it makes sense. In the last 10 weeks, PYPL has only printed three up weeks, leading to an overall negative slope across the period. Beyond that near-term point, shares have lost almost 39% of value in the past 52 weeks. As they say in baseball, PayPal could be due.

However, just like our national pastime, superstitions about being due is not a great tactic for consistent success on Wall Street. If all players were owed a big play after an extended slump, we’d never see anyone designated for assignment (basically being demoted from the main team). In reality, we see former studs fade into obscurity all the time.

I’m not suggesting that PYPL stock will collapse. Nevertheless, it’s rather obvious from the volatility skew (for the June 12 expiration date) that smart money traders aren’t willing to lever up on the bull case. Instead, they’re very much protecting against the risk of downside volatility.

By definition, the volatility skew identifies implied volatility (IV) across the strike price spectrum of a given options chain. Since IV reflects the kinetic potential of a security at the affected strike, an elevated reading beyond the normal baseline reflects greater premiums associated with covering against the implied move.

Effectively, the skew represents an insurance market. On any given day for a heavily traded security, the risk is directional: either a sharp move higher or lower. Typically, investors are concerned about covering downside risk unless they’re particularly confident in an upside move. With PYPL stock, the insurance premium is heavily geared toward out-the-money (OTM) puts.

Simply stated, if there is a tail-risk event, the smart money believes it will happen to the downside.

Triangulation of PayPal Stock Reveals Risks

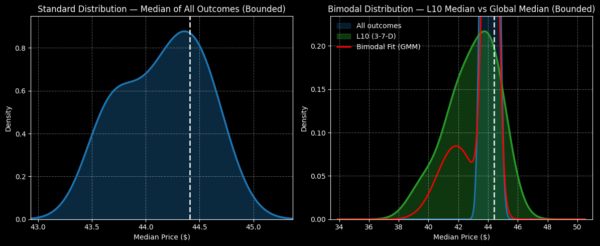

A major risk factor when trading PYPL stock involves its negative bias under a variety of market conditions. For example, if we were to take data from January 2019, a 10-week-long position is statistically likely to go underwater, with an exceedance ratio of only 45.8%. Nominally, if we assume a starting price of $44.41, the expected 10-week distribution would likely land between $43 and $45.50.

Of course, we’re not interested in trading PYPL stock randomly. Instead, we’re looking to trade the security under specific circumstances to see if there is a statistical edge. As mentioned earlier, PYPL in the last 10 weeks printed a 3-7-D sequence (three up weeks, seven down weeks, downward slope). Under this specific scenario, the exceedance ratio is glaringly worse at 35%.

Specifically, out of 40 such sequences printed on a rolling basis since January 2019, PayPal stock has only managed to rise above the starting point 14 times. Further, the expected 10-week distribution would likely place PYPL between $36 and $48. While there is some chance of an upside opportunity, the bulk of the distribution is projected to fall in negative return territory.

The caveat here is that inductive methodologies aren’t perfect and are prone to the black swan risk. Nevertheless, when we triangulate PayPal stock under 3-7-D conditions, PYPL tends to disappoint those seeking a bullish contrarian position. As such, at this moment, I’m more in favor of avoiding the name.

However, those that want to speculate may consider the 45/44 bear put spread expiring June 12. This trade requires PYPL stock to fall through the $44 strike at expiration. If it does, the maximum payout is modest at only a little above 56%.

Here’s the thing, though: the net debit required is only $64 per spread. Also, as the volatility skew demonstrates, we’re probably not looking at a collapse event. It’s just that if a big magnitude move were to occur, the smart money believes that the odds favor collapse as opposed to a rip higher.

With the above bear spread, we would just be looking to snag some profits off a disappointing slide. If that doesn’t sound appealing, PayPal stock might not be a great trading candidate for your needs.

Leave a Reply