You don’t have to look far to see why investors are apprehensive about electric-vehicle manufacturer Rivian Automotive (NASDAQ: RIVN). While the company has made great strides in providing a compelling alternative to Tesla (NASDAQ: TSLA) vehicles, the market is essentially discounting Rivian’s future in favor of its present challenges. As such, a paradigm shift in pricing for RIVN stock may not happen till later.

Table of Contents

And what exactly does later mean? Perhaps in late 2027, when Rivian’s competitively priced R2 potentially enters mass production. Until then, trading could be incredibly choppy for RIVN stock as investors balance the possible viability of the rewards versus the actual risks undergirding the brand.

Recently, the EV manufacturer’s first-quarter earnings demonstrated the frustrating case behind RIVN stock. While revenue hit $1.38 billion — which, of course, is a tangible metric tied to real demand — Rivian incurred a net loss of $416 million. Sure, the loss has narrowed over time but the return on equity remains deeply negative, representing a major deterrent for institutional value investors.

Another fundamental problem is stagnant delivery growth. Although Rivian sold 2,700 vehicles in February (a 7.3% increase from the 2,516 units registered in January), this figure is nevertheless a 34.1% drop from one-year ago. Beyond the downward trend, this datapoint suggests that because demand for the premium R1 platform is cooling, more pressure will be heaped on the R2 to save the brand.

That’s where investors are getting nervous about RIVN stock. You can talk about the technology and the electrification of mobility until you’re blue in the face — that’s all been priced into RIVN and other EV stocks. Right now, we’ve moved beyond the “wow!” phase into the “is-this-something-that-consumers-actually-want?” phase.

As the datapoints reveal, the jury is still out. Unfortunately, for those who are seeking stability in RIVN stock, that may not come until there is clearer evidence that the R2 will deliver the goods as promised.

Why the Smart Money Has Made Up Its Mind on RIVN Stock

If we’re going to get to the root of how RIVN stock is valued, it comes down to the tension between potential upside and actual dangers. Basically, for the price of shares — which, of course, you have to pay right now — you get the possibility of massive rewards in the future. At this point, though, these rewards are mostly pie in the sky. The dollars you forked over for RIVN? That’s very much real.

Obviously, this dynamic is the whole point of investing in the equities market; I’m not breaking any new ground by stating these facts. However, the volatility skew — particularly for the June 18 expiration date — lays bare the skepticism that traders have toward Rivian stock. Sure, the EV maker is bringing tangible positives to the table, such as the aforementioned revenue. However, the risks are that much more potent, forcing traders to pay for downside protection.

Basically, while the narrative surrounding electric mobility holds great promise, it’s also a storyline that has (probably) been priced into RIVN stock. What traders are now more apprehensive about is the capital intensity and potential dilution risks associated with Rivian’s long-term strategy. It’s not a cheap endeavor to build an automotive company, especially one that’s going to compete head-to-head with Tesla. Thus, at this point, the risks are more real than the rewards.

Going back to the volatility skew, implied volatility (IV) for far out-the-money (OTM) put options has soared relative to countervailing OTM calls. Structurally, the market is much more concerned about Rivian stock collapsing than it is about shares ripping higher. That’s a bold outlook considering that RIVN is down nearly 28% on a year-to-date basis.

Highly speculative and reasonably priced shares sometimes have a tendency to bounce higher from a sharp downstroke. However, most sophisticated traders don’t see this reversion to the mean materializing at this moment. Instead, the overriding motif is risk mitigation — but this also might be hiding an opportunity for aggressive bulls.

Taking an Inductive Look at Rivian Stock

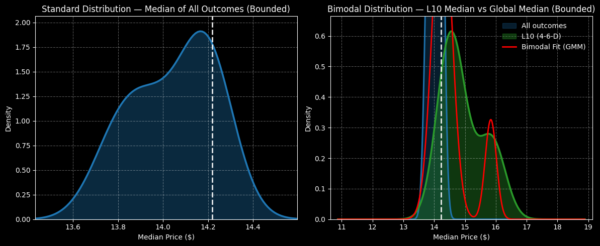

To be fair to those hedging against RIVN stock, the EV maker hasn’t really given long-side investors much to cheer about. Using a dataset going back to Rivian’s public market debut, we can calculate that the odds for a random 10-week-long position being profitable are only 50.7%. Out of 215 rolling 10-week sequences, only 109 sequences have only managed to rise above the starting point.

What’s more, the expected forward distribution isn’t all that impressive. Assuming a starting price of $14.22, you would expect a random long position in Rivian stock to land between $13.40 and $14.60. Further, the bulk of the distribution lies below spot, meaning that for most weeks, RIVN tends to give negative returns until a late break toward the end of the distribution.

Bottom line, betting on Rivian for the short term has been statistically only marginally better than a coin toss. That’s a nightmare for a debit trader. However, the key point here is that we’re not trading RIVN stock randomly but rather based on its current quantitative signal.

In the last 10 weeks, RIVN printed only four up weeks, leading to an overall downward slope. Based on an inductive analysis of other 4-6-D sequences that have flashed, we would expect the forward 10-week return under this condition to land somewhere between $13 and $17. Interestingly, under this pattern, the exceedance ratio of RIVN clocks in at 67.8%.

Obviously, Rivian is a volatile security, and so the inductive analysis above should be considered fragile. However, if you want to take a shot, the 14/15 bull call spread expiring June 18 looks intriguing. For this trade to be fully profitable, RIVN stock must rise through the $15 strike at expiration. If so, the maximum payout would be 104%. Breakeven lands at $14.49, helping to improve the trade’s overall odds.

Again, this is a high-risk proposition. But because traders are overwhelmingly prioritizing downside protection, the equivalent upside exposure is cheap. With the net debit for the above spread coming in at only $49, it’s a way to potentially make pocket change grow quickly and robustly.

Leave a Reply