It’s not difficult to have some skepticism toward financial services giant Mastercard (NYSE: MA). Granted, the company is a stalwart in the credit card business and with global transactions increasingly shifting to the digital realm, MA stock is relevant, if not boring, because of its predictability. Still, shares are down more than 14% on a year-to-date basis, and the circumstances sparking this negativity may linger.

Table of Contents

I don’t want to waste too much airtime going over the obvious, but the uncertainties surrounding the Iran conflict impose serious challenges on consumer sentiment, which in turn impacts the transactional volume that keeps the lights on at Mastercard. Given the massive size of the business, no one should expect MA stock to collapse anytime soon. However, the pivoting circumstances require a negative rerating of its market value.

Not even a relatively strong earnings report was enough to spare MA stock from the doldrums. For the first quarter, Mastercard posted earnings per share of $4.60 on revenue of $8.4 billion, beating out analysts’ consensus targets of $4.41 and $8.26, respectively. In the year-ago quarter, the card payments provider posted EPS of $3.73 on a top line of $7.25 billion.

Apparently, MA stock was a victim of the classic buy-the-rumor, sell-the-news dynamic. Investors temporarily rejoiced at the achievements, but that was also the problem — they were in the past. Unless there’s a meaningful resolution to the current geopolitical crisis, the global economy arguably faces steeper and compounded challenges.

Subsequently, the good news didn’t provide enough confidence for the market at large to reassess MA stock positively, leading to a corrective spell following the earnings disclosure. Adding fuel to the fire, even the smart money appears net cautious toward Mastercard.

Volatility Skew Signals Both Risk and Opportunity for MA Stock

For options traders, one of the most important screeners to monitor before placing any bet is the volatility skew. By definition, the skew identifies implied volatility (IV) of put and call options across the strike price spectrum of a given options chain. Since IV reflects the anticipated range of motion for the underlying security, heightened volatility readings relative to baseline may be interpreted as hedging demand.

The options lexicon can be overly complicated, but the basic philosophy here is that the volatility skew represents an insurance market. For every options-related transaction, traders have a basic choice of hedging against downside risk and upside risk. In other words, a heavily traded security could, on any given day, suffer a correction or enjoy a rally.

Obviously, no one knows for sure what will happen in the future — that’s the hallmark of a non-deterministic system. You cannot logically compel an outcome because all outcomes are based on the language of probabilities, not certainties. Because of this variable environment, the smart money isn’t smart for guessing right; it’s smart for properly managing risk.

And what does the risk management for Mastercard stock reveal? Looking at the skew for the June 12 expiration date, volatility metrics for both calls and puts near the spot price are relatively flat. Further, the skew toward the left and right tails is orderly, demonstrating no violent dislocations nor obvious panic kinks. In short, the market sees the core business undergirding MA stock as predictable.

Fundamentally, this assessment makes sense. Mastercard’s transaction volumes are diversified globally, margins are elite, the balance sheet is strong, and the business is asset-light. Structurally, you wouldn’t expect MA stock to carry a fear skew.

However, it’s still worth pointing out that the left-tail put premium is still meaningfully higher than calls. What does that say? Institutional traders are still prioritizing downside macro hedging, which, conversely, implies that the contrarian debit-based bullish position may be relatively cheap on a volatility basis.

Subsequently, if you have a reason to believe that MA stock can temporarily reverse course from its bearish trajectory, there may be a discount to be exploited.

Using Inductive Triangulation to Trade Mastercard Stock

As mentioned earlier, the equities market is a non-deterministic system. From a technical standpoint, we cannot math our way to the correct answer because the answer can never be known before it materializes. This is far different from a deterministic system. For example, two plus two will always equal four, no matter how you manipulate the wording of the question.

Given the non-determinism of Mastercard stock (or any other publicly traded security), we need to use triangulation to improve the odds of trading it profitably. Basically, we need to observe MA and its forward tendencies based on a specific signal. Through the collection of this stratified data, we triangulate the most likely pathway by extrapolating where MA stock is likely to cluster at a given point in time.

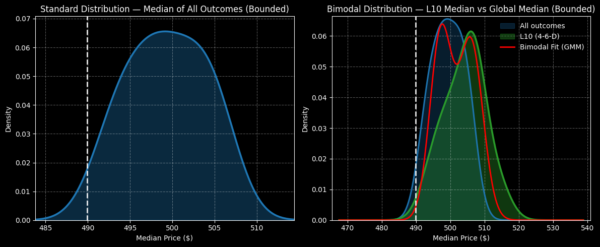

This is where we need to throw old-school methodologies like technical analysis out the window and rely on algorithms to read the massive dataset. For example, using data going back to January 2019, a random 10-week-long position in MA stock has been demonstrated to range between $485 and $515 (assuming a starting price of $489.94).

But we’re not interested in trading Mastercard stock randomly. Instead, we’re looking at the current signal. In the last 10 weeks, MA printed only four up weeks, leading to a downward slope across the period. Under this specific 4-6-D sequence, the forward 10-week distribution shifts net positively, from $480 to $524.

Moreover, from a chronological standpoint, we would expect median clustering around $510 between the third and fourth week following the 4-6-D signal. It must be said here that the inductive approach is only observational and is not perfect — Mastercard stock can easily not align with inductively calculated expectations.

Still, in a non-deterministic system, we don’t have a lot to work with besides induction. If you find the observed pattern convincing, an aggressive but rational trade would arguably be the 505/510 bull call spread expiring June 12.

For this trade to be fully profitable, the MA stock would need to rise through the $510 strike at expiration. Doing so would generate a maximum payout of 100%.

Leave a Reply