One of the more intriguing blue-chip names in the equities sector is arguably Costco (NASDAQ: COST). Looking at the aggregate performance of COST stock, the expected range of near-term outcomes is understandably positive but limited. In other words, we all know that COST enjoys an upward bias. But the question is whether the potential momentum is enough to justify a position.

Table of Contents

At the core, every major publicly traded security offers the potential for future performance in exchange for current (actual) payment. For something like COST stock, the potential is quite limited — there’s only so much that a big-box retailer can do beyond selling stuff at a competitive price. More to the point, the reward is very much tangible because we have a long history of evidence that the underlying business is viable.

On the other hand, you have speculative tech firms that may be running a lot of red ink on their financials. Here, the potential is extremely vast, in part because the actual business remains questionable. Obviously, this dynamic figures into the share price, which is why such wagers don’t command COST stock like valuations.

It’s possible that, under similar conditions, retailers like Costco might face serious downside pressure. After all, an energy crisis and geopolitical conflicts don’t exactly mix well for consumer sentiment. However, COST stock has bucked such expectations, gaining 17% on a year-to-date basis. At the same time, COST has been stuck in a sideways consolidation since February — but a solid earnings report could break the deadlock.

On May 28, Costco will release its financial results for the third quarter, with analysts looking for earnings per share of $4.92 on revenue of $69.1 billion. Given its track record, there’s a decent chance that the company will exceed expectations. If so, that could help lift COST stock from its current stalemated technical performance.

Smart Money Traders Remain Risk-Balanced on COST Stock

A key indicator that points to a risk-balanced sentiment for COST stock is the volatility skew, particularly for the June 18 expiration date. By definition, the skew identifies implied volatility (IV) across the strike price spectrum of a given options chain. Since IV represents the expected kinesis of a security, the fact that traders are willing to pay for both downside protection and upside convexity reveals uncertainty over Costco’s forward trajectory.

People can really get into the weeds when it comes to options-related lexicon. For me, the volatility skew is akin to an insurance market. For COST stock (for the aforementioned expiration date), the main priority appears to be downside protection. Essentially, the premiums for out-the-money (OTM) puts are higher on a volatility basis compared to OTM calls.

Basically, traders don’t want to risk Costco stock tumbling following the underlying company’s earnings disclosure without adequate protection. Nevertheless, the premiums for both calls and puts are being bid up for strikes north of the current spot price. This structure tells us that sophisticated market participants don’t want to risk not having any leveraged exposure should COST break the present technical deadlock.

Both outcomes are possible, and without excessive confidence in either potential trajectory, the smart money is buying insurance for both sides. Another way to look at the volatility skew is that traders are worried about unstable price discovery. Because of the dynamic fundamental environment, it’s very possible that COST stock could materially detach from the current equilibrium.

This point underscores my earlier statements about premature presuppositions of smart money prescience. Yes, it is rational to assume that professional traders are better stock pickers than the average Joe or Jane, particularly because they trade more upstream to the custody of information (i.e., they’re not reading Motley Fool articles because Motley Fool is writing articles about them).

However, just because auto insurance premiums rise doesn’t necessarily mean an auto accident is more likely to occur. While the skew provides an interesting sentiment snapshot, it doesn’t give us a probability of what might happen next.

For that, we can turn to an inductive forecasting model.

Reading the Tealeaves for Costco Stock

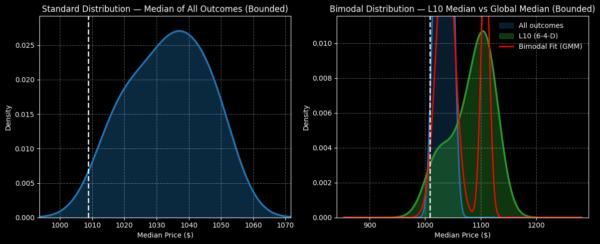

Earlier, I stated that COST stock enjoys an upward bias. Specifically, using a dataset going back to January 2019, the odds that a random 10-week-long position will end up in the black are 71.7%. This figure is calculated from 261 rolling 10-week sequences out of a total of 364 sequences that crossed above the starting point. By distribution, we would expect COST to range between $990 and $1,070 (assuming a starting price of $1008.79).

Now, if we were to assume that Costco can deliver the goods for fiscal Q3, one of the more intriguing ideas to consider is the 1080/1100 bull call spread expiring June 18. For this trade to be fully profitable, Costco stock would need to rise through the $1,100 strike at expiration. That’s a little more than a 9% move from the current spot price, which is awfully ambitious.

Even the breakeven price of $1,084.30 is 7.49% above spot, which seems like a Hail Mary for COST stock. Subsequently, the probability of profit for this trade is defined at only 18.2%. This makes sense as $1,084 would be beyond the expected aggregate range of COST.

Still, here’s where it gets interesting. In the past 10 weeks, Costco stock printed six up weeks but incurred a downward slope. Under this rare 6-4-D sequence, the expected distribution (based on an inductive analysis of prior 6-4-D patterns) would approximately land between $950 and $1,200.

Admittedly, you would be incurring greater risk here, but the reward tail conspicuously reaches further (to $1,200 instead of $1,070). In addition, probability density would peak at $1,100, right where the aforementioned second-leg strike sits.

Yes, Black-Scholes-related forecasting models may assign an extremely low probability for the above spread to be fully profitable. However, under an inductive framework, COST stock could be favorably mispriced.

Leave a Reply