From an ordinal perspective, Lowe’s Companies (NYSE: LOW) could be viewed as a discount. Currently, LOW is trading at a trailing-year earnings multiple of 20.46, noticeably lower than the 22.11x seen at the end of January. Back then, the underlying security traded hands at $267.06, meaning that against this relative benchmark, the stock is down 9.23%.

Table of Contents

Given that the company offers a dividend yield of 1.98% — and has rewarded shareholders with 54 consecutive years of dividend increases — the math seems to make a lot of sense. No, Lowe’s is hardly what you would call an exciting opportunity. However, as a defensive consumer discretionary play, it provides a sort of safe haven amid severe geopolitical uncertainties.

Unfortunately, it’s these uncertainties that make the idea that LOW represents a discount a tough pill to swallow. While there have been times in years past when Lowe’s exchanged hands at a richer multiple, that paradigm involved a global economy that wasn’t mired in a hot conflict with Iran. Today, we cannot say the same thing. Because the fundamental sentiment regime has clearly shifted, we need some other mechanism to discover value (if any).

Speaking of the fundamentals, one of the biggest headwinds impacting the company and its stock is the stalled housing turnover rate. With high mortgage rates, recent homebuyers essentially suffer from the “lock-in effect.” As The Wall Street Journal pointed out, Lowe’s has remarked that these same folks are also reluctant to remodel. That makes sense given that financing costs would be higher compared to prior low-interest-rate environments.

So, should investors avoid LOW altogether? While that may be the popular conclusion, the contrarian take may see the potential for forward asymmetry. Basically, if mortgage rates decline against expectations, one of the subsequent downwind events could be a rise in housing transactions. If so, remodeling demand may also spike, which historically drove Lowe’s revenue acceleration.

Of course, that’s more of a longer-term speculative perspective. For those who are a bit more on the impatient side and desire to frontload possible rewards, there’s an intriguing options play at hand.

Using Inductive Math to Exploit a Possible Mispricing in LOW Stock

It shouldn’t be a controversial point that every security that has traded for some time features a natural performance bias. For example, a cryptocurrency-based security could see a series of wild price discoveries, punctuated by periods of relatively muted activity. On the other end, a defensive investment like Lowe’s stock may feature a slow-and-steady trend.

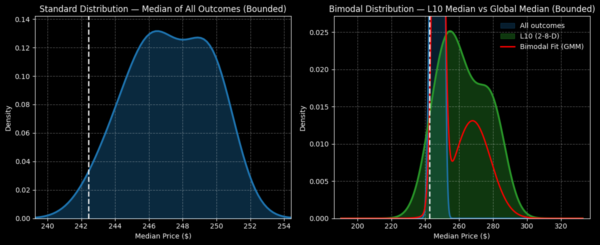

Perhaps predictably, when we look at random 10-week holds for LOW, the security features a clear upward bias. Using a dataset from January 2019, a 10-week-long position (assuming a starting price of $242.42) would likely see the stock end up in a distribution between $239 and $255. Further, the exceedance ratio — or the likelihood that LOW will end up in the black over a 10-week period — stands at 61.5%.

It doesn’t really get better than that. If you were to buy Lowe’s stock a hundred times right now, you’d expect to be profitable about 62 times over the next 10 weeks. While that does sound like easy money, the problem is that in most cases, you would expect LOW to reach only $246.

Sadly, there’s only one debit spread that expires around 10 weeks from now with a full-profitability target of $246 or lower. What’s more, the maximum payout for this spread — once you fork over the $1,600 net debit — is only 25%. Nominally, your profit would come out to only $400, a very undesirable risk-to-reward ratio (in my opinion).

Fortunately, we’re not interested in trading Lowe’s stock in the aggregate. Instead, we’re looking to trade Lowe’s stock based on a specific signal. And this signal statistically leads to a far different distribution than what we would expect as an aggregate play.

In the last 10 weeks, LOW printed only two up weeks, leading to an overall downward slope. Ordinarily, this quantitative signal would be interpreted bearishly. However, this 2-8-D sequence tends to yield a dramatically bullish forward 10-week distribution. In the same dataset mentioned above, the stock demonstrates a tendency to land between $220 and $305.

If that expectation were to play out again, LOW stock options would theoretically be favorably mispriced. Under observed baseline conditions, the market is pricing Lowe’s stock with an expected peak probability density at around $246. However, under the current 2-8-D condition, peak probability would reach around $254.

Even better, the probabilistic distribution would still be elevated in a range between $260 and $280. Thus, I see an opportunity for hardened speculators to push the needle.

Looking at $270 as a Potential Sweet Spot

While it’s an awfully ambitious idea, those who are willing to throw caution to the wind (but in a rational manner) may consider the 260/270 bull call spread expiring June 18. This transaction involves buying the $260 call and selling the $270 call simultaneously on a single ticket.

Transactionally, you would be paying a net debit of $285 per spread. Should LOW stock rise through the $270 strike at expiration, the maximum payout would clock in at $715. That means your maximum (capped) payout would be nearly 251%. Breakeven lands at $262.85, adding some margin of error for this spread.

Obviously, the above bull spread is mostly justified through the inductive process that identifies $270 as a realistic target. Induction just translates to pattern recognition: we observe in the past that the 2-8-D sequence generally leads to a sizable upside performance compared to the aggregate.

Still, the major caveat in this analysis is that, while the uniformity of nature —the assumption that the future will behave like the past — is a useful tool, it is not a foolproof one. Just because you see a thousand white swans does not mean all swans are white. As soon as a black swan appears, the inductive assumption immediately implodes.

Nevertheless, the philosophical dilemma is that any forecast about the unknown future is necessarily inductive. No one has proven that a market signal logically necessitates a particular outcome. In this case, induction is arguably our best weapon — and right now, it’s telling us there’s a solid chance Lowe’s stock is mispriced.

Leave a Reply