NetEase (NASDAQ: NTES) really isn’t for the faint of heart. Although the Chinese technology firm — which specializes in video game publishing — has seen its equity perform reasonably well over the past year, in recent sessions, NTES stock appears troubled. In the past month, the security has slipped almost 12%, which is not the sign of confidence you want ahead of fourth-quarter earnings, scheduled to be released on Wednesday before the market opens.

Table of Contents

Wall Street analysts are looking for NetEase to post earnings per share of $1.85 on revenue of $4.10 billion. In the year-ago quarter, the company posted EPS of $2.07 on revenue of $3.66 billion. At the time, the gaming specialist beat the EPS estimate of $1.77 but fell short of the sales target of $3.74 billion.

Overall, NetEase presents a very shaky earnings history. Generally speaking, it tends to beat expectations for the bottom line. Unfortunately, the same cannot be said about the company’s top-line performance. Since Q3 2022, NetEase has only beaten revenue expectations a total of four times. That’s not going to impress investors. Unsurprisingly, in the past five years, NTES stock has dipped 7%.

Thanks to its shoddy financial history, the smart money is prudently prioritizing downside insurance. But because of this tilt, there could be an opportunity for ultra-aggressive contrarians.

Volatility Skew Reveals Where the Priority is for NTES stock

One of the most important first-order analyses readily available to retail traders is volatility skew. This screener identifies implied volatility (IV) — or a stock’s potential kinetic output — across the strike price spectrum of a given options chain. For the March 20 expiration date, the skew shows a clear prioritization of smart money traders insuring against downside movements.

First, on the lower strike price boundaries, both put and call IV curve upward, with IV pricing consistently exceeding that of its call equivalent. These far out-the-money (OTM) puts reflect heightened demand to defend against downside tail risk. In other words, a non-trivial possibility exists that a sharp correction could materialize in NTES stock.

Second, on the upper strike boundaries, we also find put and call IV curve upward. Generally speaking, put IV is also priced at a premium relative to calls. This setup effectively serves as a mechanical short position, possibly as a means for institutional investors to protect their actual long exposure.

To be fair, it’s significant that sophisticated market participants are still involved in NTES stock instead of outright selling the security. Still, the overriding message here is protecting the rear flank.

Nevertheless, it’s important to state that volatility skew doesn’t reveal absolute truths. It’s not that the smart money is directionally biased toward the downside (although that could be the case). Rather, the skew is saying that the risk of not protecting against downward movement is greater than the magnitude of reward for getting the upswing right.

What’s fascinating here, though, is that bullish expression through call options is likely to be cheap on a volatility basis. If we have reason to believe that NTES stock could indeed move higher, it could be considered a discount.

Establishing the Parameters of the Trading Floor for NetEase Stock

While we now have a general understanding of smart money sentiment from the volatility skew, we’re still at a loss as to how this translates into actual price outcomes. For that, we may turn to the Black-Scholes-derived expected move calculator. Wall Street’s standard mechanism for pricing options projects that for the March 20 expiration date, NetEase stock may land between $110.07 and $135.41.

Where does this dispersion come from? Black-Scholes assumes a world where stock market returns are lognormally distributed. Under this framework, the above range represents where NTES stock may symmetrically land one standard deviation away from spot (while accounting for volatility and days to expiration).

Essentially, what the model is saying is that in 68% of cases, we would expect NTES stock to trade somewhere within the prescribed range when March 20 rolls around. That’s a reasonable assumption, if only because it would take an extraordinary catalyst to drive a security beyond one standard deviation from spot. Still, we’re left with a rather sizable peak-to-trough range of 23%.

At this point, we have reached the practical limit of first-order analyses. We now know through volatility skew what the smart money may possibly be thinking — and how these traders’ orders may disperse based on the Black-Scholes model. But what we don’t have is where NTES is most likely to end up.

What we have here is the search-and-rescue (SAR) dilemma. Basically, an SOS signal went out somewhere in the Pacific Ocean. Through Black-Scholes, we can narrow down the search radius over a large patch of water. Unfortunately, we don’t have enough resources to conduct a full-scale search for one shipwrecked survivor.

At some point, we must graduate from observed data (first order) to theoretical inference (second order). That’s where the Markov property comes into view.

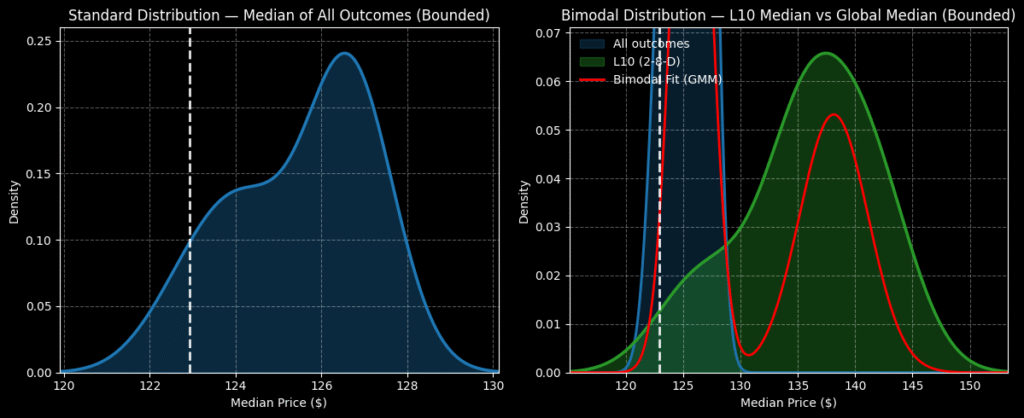

Using Science to Narrow Down the Probability Space

Under Markov, the future state of a system depends entirely on the present state. Colloquially, forward probabilities should not be calculated independently but be assessed in context. Regarding the SAR analogy, different ocean currents — such as choppy waves versus calm waters — can easily influence where a shipwrecked survivor is likely to be found.

Here’s how we can use the Markov property for NetEase stock. In the last 10 weeks (which we’ll define as the “current state”), NTES printed only two up weeks, leading to an overall downward slope. There’s nothing special about this 2-8-D sequence, per se. However, this quantitative signal represents a specific type of ocean current. Any survivor found in these waters will likely drift in a distinct way compared to if another current type were involved.

From here, we will use enumerative induction to estimate where NTES stock may drift over the next 10 weeks based on the patterns associated with prior flashings of the 2-8-D sequence. We’ll also use Bayesian-inspired inference to help estimate the likely range (due to limited sample sizes preventing pure reliance on induction).

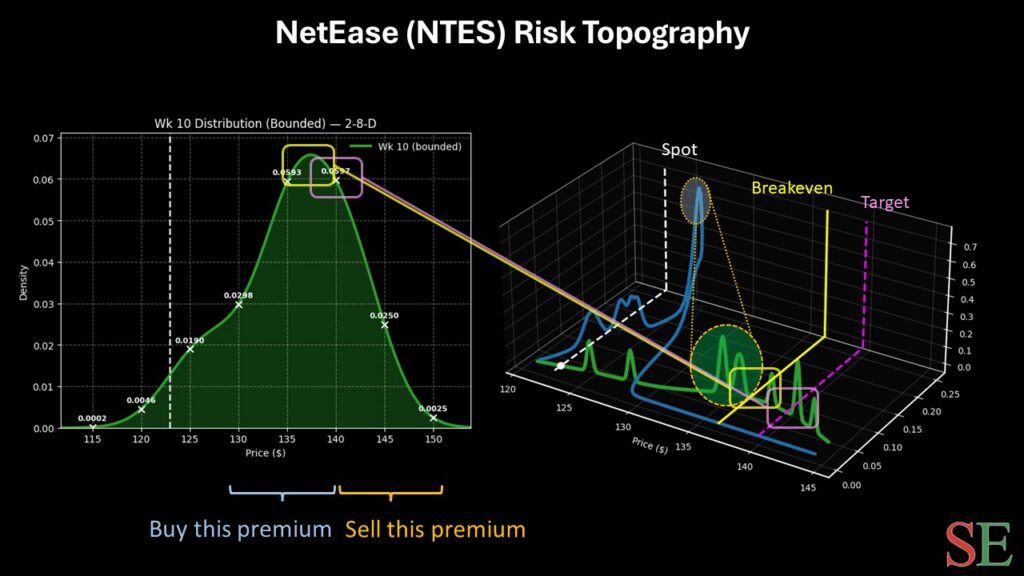

If you accept the theoretical premise of the Markov approach, we can calculate that NTES stock may land between $110 and $160 over the next 10 weeks. Probability density will likely peak somewhere between $135 and $140, thus significantly narrowing the probability space.

Based on this market intelligence, I’m very tempted by the 135/140 bull call spread expiring March 20. For this wager to be fully profitable, NetEase stock must rise through the $140 strike at expiration, which is admittedly an ambitious target. If it does trigger this level, you’re looking at a maximum payout of nearly 178%.

Breakeven lands at $136.80, which helps improve the probabilistic credibility of this trade. No, it’s not a wager for the faint of heart. However, with the prioritization focused on protecting against downside volatility, there’s a tempting avenue here to go contrarian.

Leave a Reply