Celsius (NASAQ:CELH) may represent one of the more popular entries in the ultra-competitive fitness and energy drink segment, but that hasn’t always translated into solid market performances. Indeed, CELH stock is emblematic of the non-ergodic nature of high-powered growth stocks. While security has nearly doubled in value over the past year, it’s down almost 21% over the past six months.

Table of Contents

Wall Street analysts will be looking for earnings per share of 19 cents on revenue of $638.48 million. In the year-ago quarter, Celsius posted EPS of 14 cents on revenue of $332.2 million. These figures beat the consensus targets of 10 cents and $327.02 million, respectively. Overall, Celsius enjoyed a strong performance earlier this decade, but in recent years, the misses — particularly in the growth department — have piled up.

This year, it’s down 3%, a byproduct of losing roughly 16% in the past 30 days. Unfortunately, the red ink stunted what was otherwise looking like a promising rally. It also raises the stakes ahead of the beverage maker’s fourth-quarter earnings report (scheduled for release on Feb. 19).

It’s only natural, then, that investors are concerned about what the company can deliver for Q4. However, if smart money sentiments are anything to go by, CELH stock could present an intriguing contrarian opportunity for the bulls.

Volatility Skew May Be Tipping the Hand for CELH Stock

One of the most important first-order (observational) analyses to consider for optionable securities is volatility skew. This screener identifies implied volatility (IV) — or a stock’s potential kinetic output — across the strike price spectrum of a given options chain. For the Feb. 20 expiration date, the skew shows a noticeable tilt toward upside convexity.

Specifically, the upper strike price boundaries show call IV pricing rising higher and simultaneously being priced well above put IV. This setup indicates that at the tails, a heightened premium exists for covering sizable upswings — and the smart money is willing to pay it.

To be fair, on the lower strike boundaries, put IV rises above its call equivalent, indicating a protective posture against downside tail risk. However, call IV also rises at the lower boundaries, thus making the gap between the two premiums relatively modest. Therefore, the overall posture appears to be optimistic, with smart money traders prioritizing the potential rewards of being right to the upside rather than protection against southbound volatility.

It should be noted that near the spot price, both call and put IV pricing is relatively muted. So, the atmosphere isn’t necessarily urgent or tense. Such a framework effectively provides information by omission. Because CELH stock has performed rather poorly in recent sessions, the priority should be downside protection. But we’re not getting that kind of pensive posture, which may offer a contrarian proposition.

Also, it’s worth noting that for the March 20 expiration, the smart money isn’t overwhelmingly protective. That’s why I’m thinking there could be an opportunity here.

Establishing the Trading Parameters of Celsius Stock

While we now have a basic understanding of smart money sentiments from the volatility skew, we still need to know how this translates into actual price outcomes. For that, we may turn to the Black-Scholes-derived expected move calculator. Wall Street’s standard mechanism for pricing options projects that for the March 20 expiration date, Celsius stock may land between $36.88 and $51.62.

Where does this dispersion come from? Black-Scholes assumes a world where stock market returns are lognormally distributed. Under this framework, the above range represents where CELH stock may symmetrically land one standard deviation away from spot (while accounting for volatility and days to expiration).

Basically, the model asserts that in 68% of cases, we would expect CELH stock to trade somewhere within the prescribed range in 35 days. That’s a reasonable assumption, if only because it would take an extraordinary catalyst to drive a security beyond one standard deviation from spot. Still, we’re left with a rather sizable peak-to-trough range of 40%.

At this point, we’ve really reached the maximum utility of first-order analyses. While we have a list of how uncertainty is priced, we have no idea if that pricing is accurate, for lack of a better word. Plus, we’ve been looking at data that everybody on Wall Street has access to. That’s not edge; that’s just being at parity with the baseline.

We are faced with the classic search-and-rescue (SAR) conundrum. While Black-Scholes has identified that a distress signal has gone out somewhere in the Pacific Ocean, the shipwrecked survivor could have drifted anywhere within the prescribed search radius.

Since our limited resources prevent us from conducting a full-scale search for one survivor, we have to be strategic with our efforts. That’s where the Markov property comes into frame.

Using Science to Narrow Down the Probability Space

Under Markov, the future state of a system depends entirely on the present state. Colloquially, forward probabilities should not be calculated independently but be assessed in context. Regarding the SAR analogy, different ocean currents — such as choppy waves versus calm waters — can easily influence where a shipwrecked survivor is likely to be found.

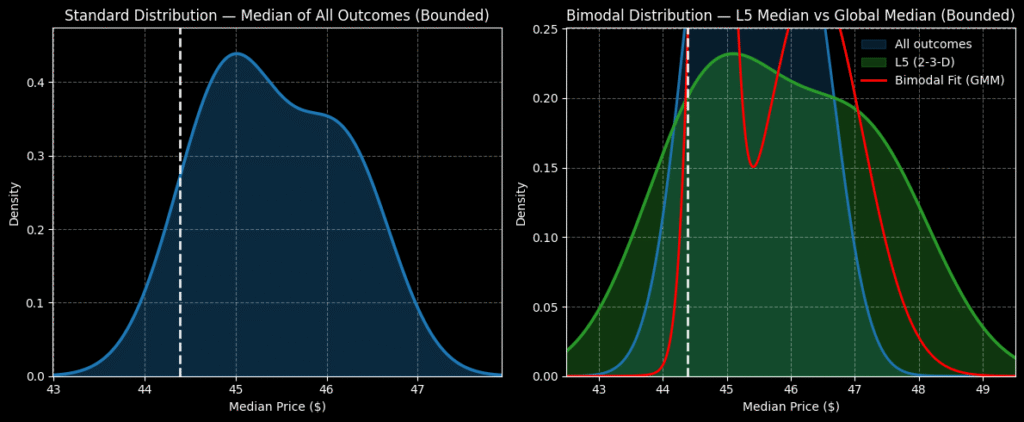

Here’s how the Markov property can be used to help us trade Celsius stock. In the past five weeks, CELH printed only two up weeks, leading to an overall downward slope. There’s nothing special about this 2-3-D sequence, per se. However, this quantitative signal represents a specific type of ocean current, and shipwrecked survivors caught in these waters would be expected to drift in a distinct manner.

How that drift pans out can be calculated using a combination of enumerative induction and Bayesian-inspired inference. The idea is that we use past analogs of the 2-3-D sequence to determine median drifting tendencies over the next five weeks. We then apply this projected rate to the current spot price to map out a potential forward pathway.

Per David Hume’s famous critique, the future is not logically compelled by the past. That’s a critique that applies to any inductive process, which would especially include fundamental and technical analysis. However, it’s my theory that the stock market is naturally Markovian and that the above second-order analysis respects the influencing agency that different market structures can impose on forward outcomes.

Assuming that you accept the premise, CELH stock would likely trade between $42 and $50 over the next five weeks, with probability density peaking between $44 and $47.70. This range gives us a much narrower probability space to target compared to the wide dispersion of Black-Scholes.

With this market intelligence, I’m tempted by the 45.00/47.50 bull call spread expiring March 20. This trade requires Celsius stock to rise through the second-leg strike at expiration to be fully profitable, which amounts to a payout of almost 107%. Breakeven lands at $46.21, helping to improve the trade’s probabilistic credibility.

Leave a Reply