AbbVie (NYSE:ABBV) historically represents a favorite among conservative buy-and-hold investors for good reason. Fundamentally, unless you envision a future where humans don’t get old and don’t get sick, AbbVie’s core healthcare business should be permanently relevant. From a financial perspective, ABBV stock delivers solid returns — having gained almost 28% in the trailing year — while also posting a 3.2% dividend yield.

Table of Contents

So, with AbbVie off to a slow start to 2026, it’s a natural signal to at least consider the contrarian bullish position. What’s more, ABBV stock has been deflated for some time. In the past 30 days, it’s off course by more than 5%. Since the close of the Oct. 1 session, the equity is down roughly 12%.

Historically, the healthcare juggernaut tends to bounce back from extended downside, and that’s really the narrative that we have before us. Not only that, a positive surprise for its upcoming fourth-quarter earnings report could reinvigorate sentiment for ABBV stock.

Analysts are looking for earnings per share to hit $2.92 on revenue of $16.39 billion when AbbVie discloses results on Feb. 4. In the year-ago quarter, the company posted EPS of $2.16 on revenue of $15.1 billion, missing the consensus EPS target of $2.26 but exceeding the sales forecast of $14.83 billion.

Still, despite the mixed results, ABBV stock popped higher following the disclosure. While it’s impossible to say with absolute certainty how events may transpire two weeks from now, the setup is awfully enticing.

How the Options Market Offers a Contrarian Skew for ABBV Stock

One of the more insightful screeners that short-term traders should consider is volatility skew. This readout shows how implied volatility (IV) — which reveals the expected kinesis of the target security based on actual order flows — differs across various strike prices for the same expiration date.

What we’re looking for is the volatility smile. In the case of ABBV stock, puts for the Feb. 20 options chain feature a higher IV in the lower strike price ranges than calls, meaning that the smart money is effectively paying a more robust premium for downside insurance (or outright bearish speculation).

On the flipside, the above dynamic leaves call options relatively underpriced relative to puts. Therefore, if we have a good reason to go with the contrarian trade, ABBV stock could be mispriced in our favor. Essentially, we could take advantage of an expectational arbitrage.

We’ll get there in a second. For the Feb. 20 expiration date, the Black-Scholes model — which is Wall Street’s standard mechanism for pricing options — reveals that the expected move for ABBV stock is between $202.96 and $229.12, representing a 6.05% high-low spread from the spot price.

At first glance, this dispersion seems insightful, and honestly, it provides the parameters of the trading battlegrounds. However, we’re left in the dark as to where in this wide spectrum of prices ABBV stock is most likely to congregate at expiration.

Primarily, the challenge is that Black-Scholes assumes a perfect, risk-neutral world where outside context doesn’t influence forward probabilities. So, in this world, a three-pointer is always more difficult to make than a layup due to the greater distance to the basket.

However, real-world situations don’t work so neatly. After all, the opposing team isn’t just going to let you walk up and get an uncontested shot in. Due to different dynamics found in actual games, the probability of a scoring effort is best determined by context rather than distance.

Leveraging the Markov Property for the Financial Markets

It might seem that I’m critical of the Black-Scholes model, which would be an untrue claim. What makes Black-Scholes so special is that it’s a uniform, standard template that everyone has essentially agreed to use. When I say that it doesn’t consistently reflect reality, that is a well-known limitation. However, before we start nitpicking its findings, we must first have a frame of reference.

Like it or not, Black-Scholes provides that frame of reference. Still, as analysts, our job is to determine whether the model is the most optimal representation of forward probabilities for a given options chain. In my opinion, certain ABBV call options could be underpriced, allowing us to possibly scalp some profits.

Where the mispricing becomes discernible is through a second-order analysis using the Markov property. Under Markov, the future state of a system depends only on the current state. Put simply, everything is contextual. Going back to my earlier basketball analogy, a three-pointer could actually be the statistically easier shot to make if the route to a layup is heavily defended.

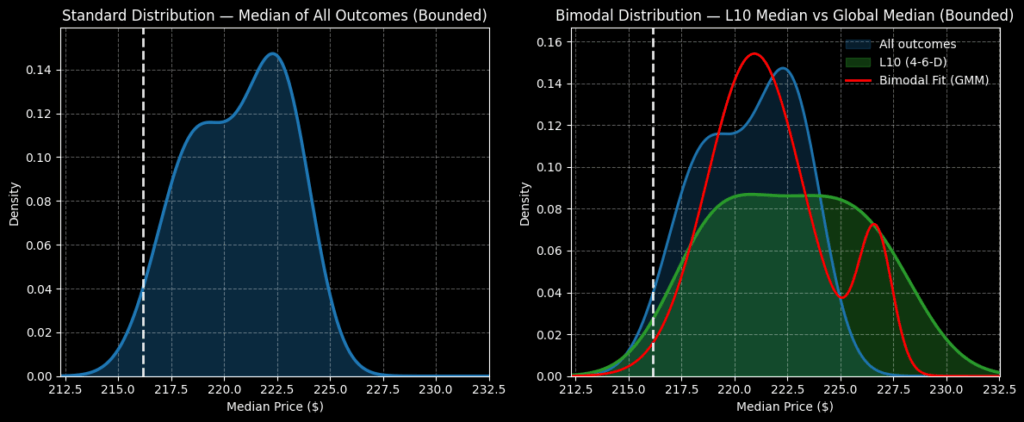

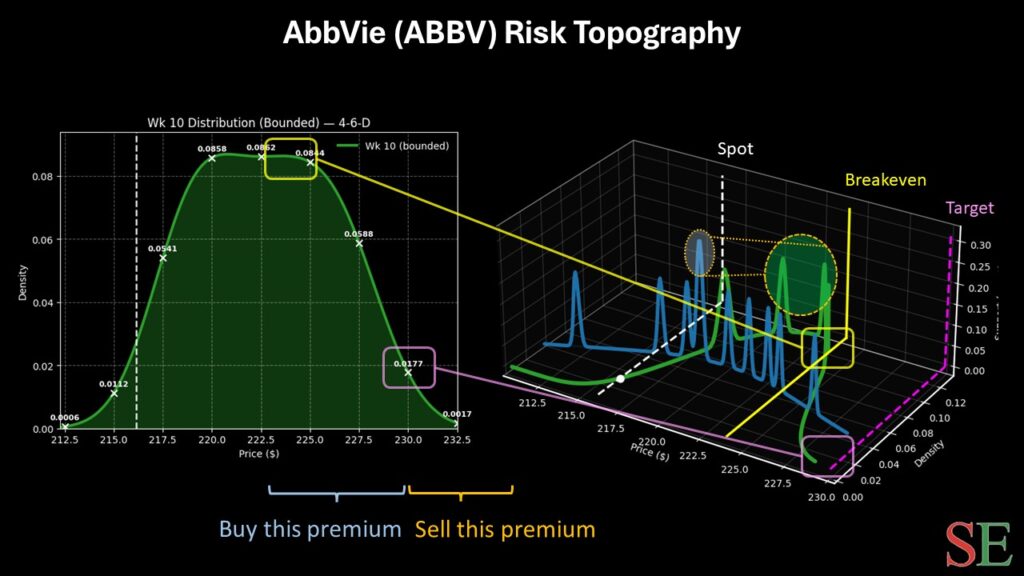

When it comes to ABBV stock, the current context is that the security, in the last 10 weeks printed only four up weeks, thereby leading to a downward slope. Under this quantitative setup, the forward 10-week returns would likely land between $212.50 and $232.50.

To be fair, this spectrum is wide and doesn’t materially improve from the expected dispersion of between $203 and $229 under the Black-Scholes model. But the beauty of the Markovian hierarchical approach is probability density. Over many trials of the 4-6-D sequence (44 rolling trials since January 2019), we would expect ABBV stock to cluster most prominently between $218 and $226 over the next 10 weeks.

Even better, this distribution wouldn’t be expected to shift dramatically over the next five weeks, coinciding with the Feb. 20 options chain. Plus, the speculation is that a better-than-expected earnings report could help boost momentum, making ABBV stock a compelling contrarian candidate.

Letting the Numbers Build the Trade

Armed with the market intelligence above, the trade that would appear to make the most sense is the 220/230 bull call spread expiring Feb. 20. This wager involves two simultaneous transactions on a single ticket (execution): buy the $220 call and sell the $230 call, for a net debit paid of $402 (the most that can be lost).

Should ABBV stock rise through the $230 strike at expiration, the maximum profit would be $598, a payout of nearly 149%. Breakeven lands at $224.02, enhancing the trade’s probabilistic credibility.

To be sure, the $230 strike falls near the bullish end of the distribution, which means it’s an awfully ambitious target. However, the breakeven price sits close to the center of peak probability density under 4-6-D conditions. With any luck, AbbVie may deliver a strong earnings print, which could make this spread a lucrative proposition.

Leave a Reply