After lagging the discount retail sector for much of the past five years, Burlington Stores Inc. (NYSE: BURL) stock may finally be ready for a breakout. The off-price apparel retailer, known for its value-focused merchandise and national store footprint, has recently shown signs of renewed strength that could make it one of 2026’s comeback stories in retail.

Table of Contents

BURL stock is up roughly 6% in the last 12 months, a modest recovery relative to the broader market and industry benchmarks. But the short-term trend tells a more encouraging story—shares have climbed 13.8% in the 30 days ending January 14, 2026, suggesting that investors may be beginning to price in improving fundamentals ahead of next quarter’s earnings report.

For long-term shareholders, the recent rally is a welcome change. The discount retail sector has delivered resilient performance in a high-inflation environment—chains like TJX Companies (NYSE: TJX) and Ross Stores (NASDAQ: ROST) have capitalized on value-conscious shoppers shifting away from full-price retailers. However, Burlington has been an outlier, and not in the best way. Over the past five years, BURL has posted a total return of about 19.8%, while TJX has surged more than 145% over the same period.

So what’s been holding Burlington back? And what could make 2026 different?

A Business in Need of a Refit

Burlington’s challenges over the past several years are well known. The company’s store base underperformed peers, its merchandising strategy lacked consistency, and its supply chain fell behind modern standards. As logistics costs soared and inventory management became a critical differentiator, Burlington’s outdated distribution centers became a drag on both margins and execution.

These issues left the retailer unable to fully capture the pandemic-era boost that benefited other discount chains. While competitors implemented technology-driven inventory planning and faster restocking models, Burlington’s lower operational efficiency limited its ability to meet shifting consumer demand.

Though management acknowledged the operational gaps, execution on turnaround initiatives took time. Investors grew restless, and the stock lagged despite rising net sales and store expansion.

But the tide may finally be turning.

Earnings Growth Suggests Progress

Despite its uneven stock performance, Burlington’s underlying financial improvement has been notable. Over the past two years, earnings per share (EPS) have grown more than 30%, showing that cost-control measures and store optimization are making an impact. Analysts forecast another 16.7% EPS growth in 2026, pointing to accelerating profitability even in a competitive retail landscape.

The company has benefited from its sharpened focus on off-price apparel assortments, tighter cost management, and operational streamlining. Burlington’s model—with limited e-commerce exposure and reliance on in-store “treasure hunt” experiences—also aligns with the trends that have supported TJX and Ross. As consumers trade down, Burlington’s value-driven mix could help it capture renewed foot traffic and margin expansion in 2026.

However, investors should note that optimism is already reflected in valuations. The stock currently trades at a price-to-earnings ratio (P/E) of roughly 34x, which is well above its historical average and well above the apparel retail sector average, according to Yardeni Research. That premium valuation implies that much of Burlington’s recovery story may already be priced into the stock, leaving less margin for error if growth stalls.

BURL Stock: An Ironic Buy-the-Dip Candidate

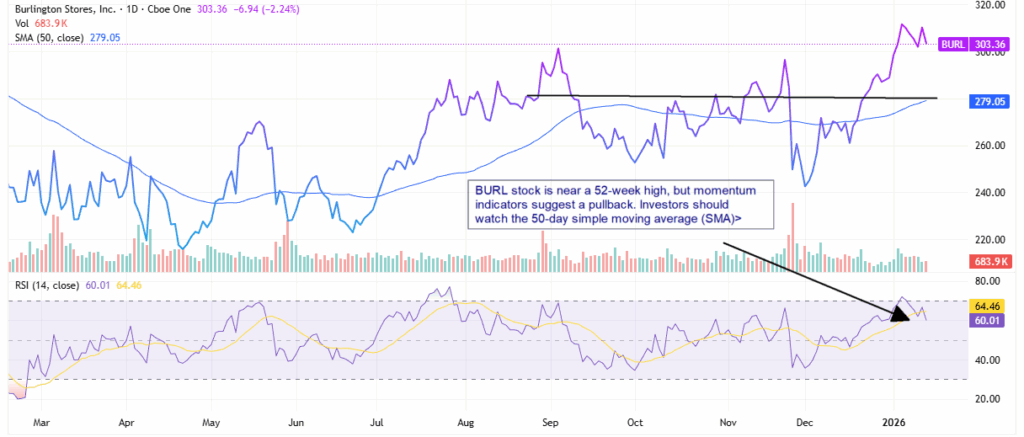

I’ve spent most of this article explaining why Burlington Stores needs a catalyst to push the stock higher. So, it’s a little ironic to say that BURL stock looks a little extended at the moment. But that’s what the chart shows.

After the stock’s recent rally, the relative strength indicator (RSI) puts the stock in overbought territory. Plus, the MACD line (not shown) has moved from bullish and supportive to nearly flat. That suggests that short-term momentum is bearish.

That said, analysts have a consensus price target of $335.94, which offers about 11% upside. However, if the stock pulls back to its 50-day simple moving average (SMA) around $280, it will give investors nearly 10% more upside.

Strategic Tailwinds and Risks for 2026

Looking ahead, Burlington’s outlook hinges on two key drivers: operational execution and consumer resilience.

1. Supply Chain and Inventory Modernization:

The company has invested in upgrading its distribution centers, improving inventory flow, and centralizing purchasing decisions. These efforts should reduce bottlenecks and improve in-store assortment, enabling Burlington to be more responsive to shifts in demand.

2. Store Expansion and Productivity Gains:

Burlington plans to expand its store base while optimizing existing locations, moving toward smaller-format stores that deliver higher returns per square foot. This shift could enhance its long-term earnings leverage, particularly if traffic remains strong.

3. Consumer Spending Trends:

While off-price retail typically outperforms in uncertain economic environments, sustained wage growth and moderating inflation could shift discretionary spending patterns. If consumers trade back up to mid-tier retailers, Burlington could see pressure on same-store sales.

4. Competitive Positioning:

The company’s main rivals, TJX and Ross, maintain structural advantages in scale and efficiency. Burlington’s growth potential depends on narrowing that gap through disciplined execution and margin expansion rather than rapid top-line growth alone.

If management delivers on those fronts, Burlington could move from being a sector laggard to a meaningful growth story in 2026. But given its current valuation, investors will expect consistent quarterly execution to justify further multiple expansion.

Conclusion: A Potential Comeback Worth Watching

As a fan of The Office I think it’s appropriate to close this article by pointing out the recurring mention of Burlington Coat Factory. The store was portrayed as a reminder that “a little money can go a long way.” That sentiment could apply again here. Burlington Stores doesn’t need to dominate the retail sector to deliver meaningful shareholder value. It just needs to keep executing.

Leave a Reply