Most investors don’t spend their mornings watching freight rates or dry bulk carriers. They watch the S&P 500, Treasury yields and whatever Nvidia happens to be doing that day. Ironically, one of the earliest clues about where those markets could be headed is often floating somewhere between Australia and China carrying iron ore.

Table of Contents

That’s why shipping stocks have always fascinated me.

They rarely lead financial headlines, yet they sit at the very beginning of the economic chain. Before factories increase production, before retailers restock shelves, before stronger earnings begin appearing in quarterly reports, someone has to move the raw materials that make all of it possible. If those ships slow down, the effects eventually ripple through manufacturers, retailers and, ultimately, stock portfolios.

Lately, shipping has started telling a story I don’t think Wall Street can afford to ignore.

Global Trade May Be Finding Its Footing

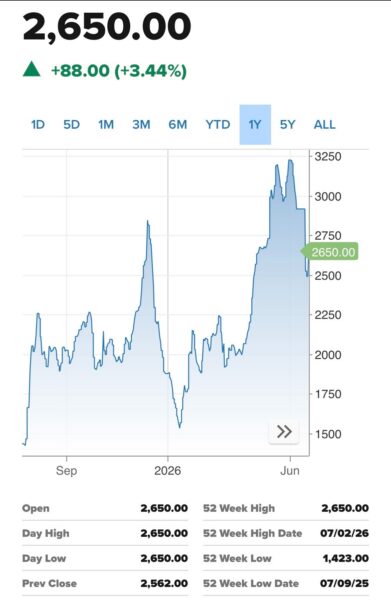

The Baltic Dry Index, one of the world’s most closely watched measures of shipping costs for raw materials, has spent the past several weeks sending mixed signals. After falling sharply from above 3,200 points to below 2,500, the index has now climbed back to 2,650, marking its third consecutive advance and its highest reading since June 24.

Rates for Capesize vessels, the massive ships carrying roughly 150,000 tons of iron ore and coal, climbed 6.2% to 3,291, supported by improving cargo activity along Australia’s and Brazil’s major export routes. Panamax rates rose 0.8%, while Supramax vessels also edged higher, suggesting the recovery isn’t confined to a single corner of global shipping.

None of this guarantees the global economy is suddenly accelerating again. It does suggest that the demand for the raw materials economies consume before factories manufacture finished goods hasn’t continued deteriorating the way many investors feared just a few weeks ago. That’s an important distinction because shipping doesn’t wait for GDP reports or corporate earnings to confirm what’s already happened. It responds to purchase orders being placed today for production that may not show up in financial statements until months from now.

Why Shipping Stocks Matter Beyond Shipping

This is where I think investors often misunderstand the industry. Shipping companies aren’t simply transporting cargo. They’re transporting information.

Every container filled with machinery, every shipment of iron ore, every cargo of coal or grain represents a business somewhere making a decision about future demand. Manufacturers don’t order raw materials because last quarter’s earnings looked good. They order them because they expect future production to justify today’s purchases.

That’s why shipping has earned a reputation as one of the economy’s earliest indicators.

When shipping volumes weaken, it often reflects businesses becoming more cautious long before consumers notice any difference. When freight demand begins stabilizing after a sharp decline, it can signal companies are regaining enough confidence to replenish inventories, restart projects or prepare for stronger activity ahead.

The message isn’t always perfect. But it usually arrives earlier than the headlines everyone else is watching.

The Market Is Watching The Same Tug Of War

The recent movement in shipping reflects the same uncertainty dominating financial markets.

Tariffs continue reshaping trade routes. Companies are still diversifying supply chains after years of geopolitical disruptions. Manufacturers remain cautious about committing capital while waiting for greater clarity on global demand.

That uncertainty explains why the Baltic Dry Index hasn’t recovered in a straight line. The one-year chart tells a far more interesting story than a simple rebound. After climbing from roughly 1,400 to above 3,200, freight rates surrendered much of those gains before finding buyers again near 2,500. The latest recovery toward 2,650 suggests investors haven’t abandoned the shipping story. They’re testing whether recent weakness represented a temporary pause or the beginning of something more persistent.

Markets behave the same way. They don’t price certainty. They constantly weigh competing probabilities. Shipping stocks are doing exactly that today.

What I’m Watching Next

Following this under-the-radar sector is dear to me because they often force me to think about the economy several months before quarterly earnings begin telling the same story.

If this recovery in shipping continues broadening across vessel classes while freight rates keep stabilizing, I’d become increasingly interested in what that implies for industrial companies, commodity producers, railroads and manufacturers whose fortunes depend on healthy trade flows. If, instead, this proves to be another short-lived bounce before freight demand resumes weakening, I’d treat it as an early reminder that optimism about global growth may have gotten ahead of itself.

Either outcome reaches much further than shipping.

By the time stronger trade appears in corporate earnings, the ships carrying the iron ore, coal and grain behind those numbers have usually completed their voyages long ago. I don’t believe shipping stocks are the next big winners. But I’ll keep watching companies like A.P. Moller – Maersk (CPH: MAERSK-B), ZIM Integrated Shipping Services (NYSE: ZIM) and Star Bulk Carriers (NASDAQ: SBLK), because they often provide one of the earliest windows into where global trade, and eventually corporate earnings, are heading.

Leave a Reply