Axon Enterprise (NASDAQ: AXON) has had a rough 2026. The stock has fallen roughly 50% from its 52-week high of $886, and currently trades around $450. That’s well below a Wall Street consensus price target north of $670, which is a 45% to 50% discount to where analysts collectively think the stock should be. That raises an uncomfortable question: is the market seeing something the analysts aren’t, or is this a setup that contrarian investors should be paying closer attention to?

Table of Contents

The answer, as with most things in investing, is both. But the weight of the evidence tilts toward opportunity.

Why the Stock Got Here

To understand the bull case, you first have to understand the sell-off. The stock’s decline isn’t a single-cause story. It’s a pile-up of several pressures hitting at once, some macro, some company-specific, and some more noise than signal.

Early 2026 saw a broad rotation out of software-as-a-service (SaaS) stocks. Investors, spooked by fears that AI commoditization would hollow out subscription software pricing power, dumped SaaS names indiscriminately. Axon, which generates an increasing share of revenue from cloud-based evidence management and AI-powered tools, got swept into that basket.

The more substantive concern is profitability. Axon’s GAAP operating income turned negative in 2025. Stock-based compensation totaled $610 million last year — nearly 60% higher than 2024 — and management has guided for another $590 million to $620 million in 2026. That kind of dilution is hard to ignore, and the market is right to hold it against the stock. At roughly 53 times forward earnings, AXON is not a cheap stock by conventional measures, even after the pullback.

What the Market Appears to Be Underpricing

Here is where the contrarian case gets interesting. While the stock has been in freefall, the underlying business has not missed a beat.

Q1 2026 was, by Axon’s own description, its strongest first quarter on record:

- Revenue came in at $807 million, up 34% year over year, marking the company’s ninth consecutive quarter of growth above 30%.

- Software and Services revenue grew 35% to $355 million.

- Connected Devices — the segment containing TASER hardware and body cameras — grew 33% to $453 million. Both segments are firing, and neither is showing deceleration.

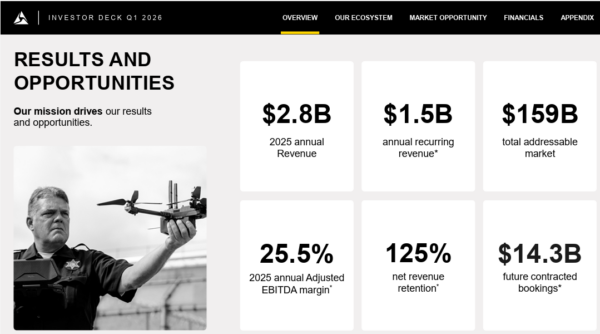

Annual recurring revenue reached $1.5 billion, up 35% year over year. Net revenue retention came in at 125%, meaning existing customers are spending meaningfully more each year. That figure has been remarkably consistent and is a strong indicator of the platform’s stickiness. When customers don’t churn and consistently expand their spend, the revenue base compounds quietly and durably.

The number that may be most underappreciated is Axon’s future contracted bookings, which hit $14.3 billion in Q1 — up 44% year over year. To put that in context: a company with a market capitalization of around $36 billion is sitting on $14.3 billion in contracted future revenue. That level of forward visibility is unusual for a growth company and provides a meaningful floor of demand that doesn’t show up in trailing earnings multiples.

New Growth Vectors That Weren’t in the Original Thesis

Many investors still think of Axon primarily as the TASER company. That framing is at least five years out of date.

Axon’s AI product revenue grew more than 700% year over year in Q1 — admittedly from a small base, but the trajectory is real. Products like DraftOne, Axon Assistant, and Axon Vision are gaining rapid adoption, and management noted on the Q1 earnings call that nearly all large domestic law enforcement agencies are now including AI tools in their purchases. AI bookings rose 140% year over year. The AI Era Plan, Axon’s bundled AI subscription offering, is pulling through additional software revenue on top of existing contracts.

Counter-drone technology is a second emerging vector. Axon’s Dedrone acquisition is contributing meaningfully and ahead of expectations, with Q1 bookings up 500% year over year and revenue up more than 300%. The market for drone detection and mitigation is expanding well beyond the law enforcement context into infrastructure protection, military support, and commercial security — markets Axon is now positioned to serve.

International revenue more than doubled in Q1, now representing 20% of total revenue. Geographic diversification matters here because it reduces dependence on U.S. federal and local government budgets, which remain a legitimate risk given ongoing scrutiny of discretionary spending.

The Honest Risks

A contrarian thesis has to be honest about what the bears are seeing. The valuation is the first issue. Even with the pullback, Axon trades at a premium that requires continued strong execution. A miss on margins or a meaningful slowdown in ARR growth would likely cause further multiple compression.

Government budget constraints are a real consideration. Axon’s core customers are law enforcement agencies funded by municipal and federal budgets, and any significant austerity push could delay contract cycles or compress upgrade timelines.

On the question of insider activity: several executives have sold shares in recent months, though it is worth noting that many of these transactions were executed under pre-scheduled Rule 10b5-1 trading plans, which are set up in advance and do not necessarily reflect a bearish view of the stock’s near-term direction.

The more telling signal may be the absence of meaningful insider buying at these levels. With the stock trading nearly 50% below analyst targets, one might expect executives to take advantage of the discount. The fact that they have not is not necessarily alarming, but it is a data point worth tracking.

The Valuation Math on a Forward Basis

Current trailing metrics make AXON look expensive. But the story changes when you look forward. Analysts are forecasting earnings per share of roughly $7.86 for 2026 and approximately $10.77 for 2027, compared to a trailing EPS in the neighborhood of $2.57. If those estimates prove out, the stock is trading at roughly 42 times 2027 earnings — still a premium, but one that looks far more defensible for a company compounding revenue at 30%-plus annually with $14 billion in future contracted bookings and a dominant position in an underpenetrated market.

The price-to-sales ratio has also compressed dramatically. Axon traded near 30 times sales at its 2025 peak. It now sits below 10 times for the first time since 2023. That is still not “value” territory, but it reflects a meaningful re-rating that may have overshot the fundamentals.

The Contrarian Read

AXON is not a value stock. It likely never will be. The argument here is not that the shares are cheap in absolute terms — it is that the gap between the operational reality of the business and the current market price has become unusually wide, driven by forces that are largely external to the core thesis.

Nine straight quarters of 30%-plus revenue growth. A $14.3 billion contracted backlog. A 125% net revenue retention rate. AI and counter-drone segments are inflecting rapidly. International revenue is doubling. These are not the characteristics of a business that deserves a 50% haircut from its highs.

The market is asking Axon to prove that its revenue growth translates into durable GAAP margins. That is a fair ask. But investors willing to give the company a quarter or two to show that proof — and comfortable with the still-premium valuation — are looking at a stock priced well below where the analyst community collectively thinks it should be, with a business executing at a high level. That combination does not come around often.

Leave a Reply