Wall Street has spent years misreading Robinhood Markets (NASDAQ: HOOD). When the commission-free brokerage burst onto the scene, critics dismissed it as a meme-stock casino. The skeptics said the company was a plaything for retail traders chasing GameStop (NYSE: GME) squeezes and Dogecoin moonshots. When the company’s crypto revenues cratered and the stock fell roughly 30% year-to-date through April, those same critics declared the thesis broken.

Table of Contents

But they’re still missing the point.

Robinhood isn’t a brokerage with a crypto problem. It’s a vertically integrated financial platform under construction. And management is flooding the zone with product launches faster than analysts can reprice the stock. The Q1 2026 earnings report brought the story to life:

- Prediction markets are hitting record contract volumes.

- IPO underwriting is coming online.

- Trump Accounts positioning Robinhood as a public-sector infrastructure vendor,

- Bitstamp is providing institutional crypto rails that most fintech competitors don’t have and can’t quickly replicate.

The company’s own CFO framed it plainly on the earnings call. Crypto represents roughly 18% of revenues, and Robinhood has “vastly diversified.” The market heard about the 47% decline in crypto revenue and sold the stock. Long-term investors who read past that headline found a business generating $534 million in adjusted EBITDA at a 50% margin, with $5.2 billion in corporate cash and a freshly authorized $1.5 billion buyback.

At roughly 46x earnings, Robinhood may be the most underappreciated super app in American fintech.

Robinhood Is Building the Financial Stack, Not Just the Trading App

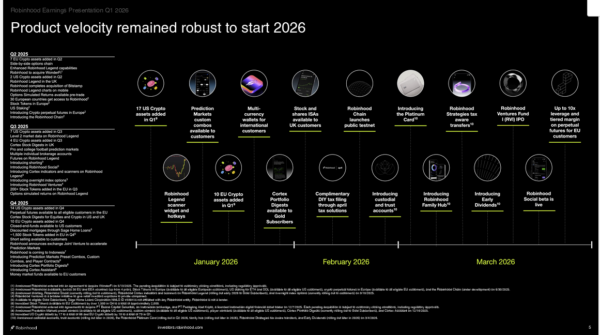

In its Q1 2026 earnings report Robinhood released a new product velocity that reads less like a brokerage and more like a platform company assembling vertical integration piece by piece.

Prediction markets traded 8.8 billion contracts in Q1, up 4% quarter-over-quarter and from essentially nothing 18 months ago. The Rothera joint venture with Susquehanna is set to launch in Q2, giving Robinhood its own prediction market exchange infrastructure rather than routing volume through third parties.

The wealth management stack is scaling simultaneously.

- Robinhood Strategies hit $1.5 billion in assets under management.

- The Gold Card now has 765,000 cardholders with $1.1 billion in balances.

- Robinhood Banking launched and rapidly accumulated $1.6 billion in balances in its first full quarter of reporting.

- Retirement accounts reached a record $27 billion in assets under custody.

- Gold subscribers hit 4.34 million, 15.8% of funded customers, and those subscribers carry roughly five times the assets of average users.

This isn’t a trading app with premium features bolted on. It’s a deposit franchise, a wealth manager, an exchange operator, and a card issuer — still being priced like it’s 2021.

Crypto Infrastructure, Not Just Crypto Exposure

Most investors still read Robinhood’s crypto exposure as beta to Bitcoin prices. That framing is increasingly outdated. The Bitstamp acquisition — completed in June 2025 — brought institutional crypto infrastructure, with 94% of Bitstamp’s Q1 2026 notional volume being institutional. That’s custody, lending, and exchange infrastructure for institutional counterparties, not retail traders reacting to price action.

Meanwhile, Robinhood is building the Robinhood Chain and has expanded to 30 EU and EEA countries with stock tokens, crypto perpetual futures, and staking. The company isn’t layering crypto on top of a brokerage. It’s using crypto rails as the foundation for cross-border financial services—a significantly different, more durable architecture than anything legacy brokerages or neobank competitors are fielding. When CEO Vlad Tenev says he wants crypto to function as “infrastructure,” the Bitstamp acquisition and international expansion suggest he means it structurally, not rhetorically.

The Chart Is Trying to Tell You Something

After peaking near $143 in September 2025, HOOD spent the better part of seven months in a sustained downtrend, breaking back below its 50-day moving average and finding a floor around $69–$70 in late April following the Q1 earnings miss. The stock’s current pattern is constructive: shares are trading near $86, back above the 50-day SMA sitting at $79, and the MACD has crossed into bullish territory with the signal line and histogram both confirming early momentum.

Volume on recent up days has been above average, consistent with institutional accumulation rather than retail short covering. The May trading update — which showed equity volumes tracking to be the highest month of the year — provided a fundamental catalyst that the technical setup was already anticipating. The prior resistance zone around $85–$90, which capped multiple rally attempts between November 2025 and May 2026, is now the level to watch as potential support. A sustained hold above that range opens the path toward retesting the $100–$110 zone.

Why the Bear Case Still Deserves Respect

No thesis comes without risks, and Robinhood’s business model carries several that are specific and material. The crypto revenue dependency, while declining as a share of the mix, isn’t gone. A prolonged Bitcoin bear market would stress transaction revenues in ways that prediction markets and Gold Card interchange can’t fully offset in the near term.

Regulation remains a persistent overhang. PFOF faces ongoing scrutiny, the Rothera joint venture is a novel structure without a regulatory track record, and event contracts have already drawn legal challenges that management acknowledged could “prevent us from offering” that product.

The Trump Accounts initiative adds $100 million in operating expense to 2026 guidance. The margin on that work is described as “small,” meaning execution risk exists if the program encounters political or logistical delays. International expansion is capital-intensive and faces entrenched local competitors.

And monthly active users actually declined year over year to 13.5 million in Q1 — a metric that matters for long-term platform monetization, regardless of how strong the Gold subscriber cohort looks.

HOOD May Be Entering Its Next Expansion Phase

Robinhood is running a platform playbook that the market is still reading as a brokerage story. With $68 billion in trailing net deposits, a 56% LTM adjusted EBITDA margin, institutional crypto infrastructure, an exchange JV launching this quarter, and a product calendar that includes banking, wealth management, and public-sector fintech — the sum of parts is growing faster than the multiple suggests. The next re-rating catalyst may already be in motion.

Leave a Reply