Life comes at you fast when you’re a leading consumer brand. Just a few years ago, Lululemon Athletica Inc. (NASDAQ: LULU) was synonymous with athleisure. In fact, the company’s signature leggings were almost like saying “Kleenex” instead of “facial tissue.”

Table of Contents

However, a confluence of factors has pushed LULU lower, and the bottom may not yet be in. Competition has emerged that offers “good enough” quality at a dramatically lower price. That plays into the inflation narrative as customers are being more “choiceful” (hint: that doesn’t include Lululemon).

All of these factors converged in the company’s Q1 earnings report for its 2026 fiscal year. The headline numbers will show a double beat. But investors didn’t believe that was nearly good enough. LULU stock dropped 8.5% to make a new 52-week low. That drop occurred with a volume nearly 5x the average.

The Numbers Behind the Headlines

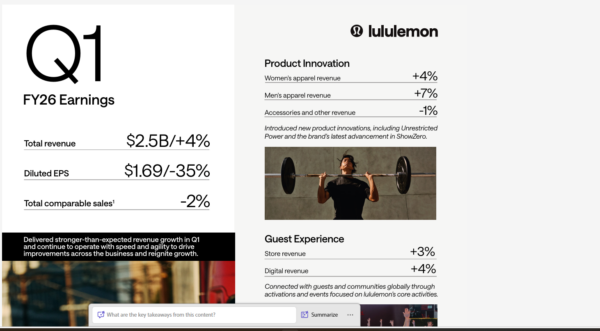

Revenue rose 4% to $2.47 billion in Q1 FY2026, but the real story is in the margins. Gross margin collapsed 410 basis points to 54.2%, and operating margin fell 730 basis points to just 11.2%. Diluted EPS came in at $1.69, down sharply from $2.60 a year ago. Management’s full-year guidance now calls for revenue of $11.0 billion to $11.15 billion — essentially flat to slightly down versus fiscal 2025.

The geographic split tells two different stories. Americas revenue fell 3% reported, or 4% on a constant-dollar basis, with comparable sales down 5% to 6%. International revenue surged 22% reported and 16% in constant dollars, led by China Mainland, which grew 30% in reported terms and 23% on a constant-dollar basis. Rest of World — primarily Europe and broader Asia-Pacific — grew 13% reported and 9% in constant dollars. International is carrying the company, but it isn’t large enough yet to offset the Americas’ drag.

A Brand Problem, not a Macro Problem

The core issue is one of brand equity. Competing with more nimble competitors means competing on price. However, that takes some of the allure out of owning apparel with that logo. It was a status symbol. Now it may be a sign that customers are paying too much for too little.

It’s important to remember that Lululemon is a premium brand that’s struggling. It’s not credible for management to cite the pressures that other retailers are noting from the lower leg of the K-shaped consumer economy. The target customers for Lululemon shouldn’t be under the same duress.

It has echoes of Nike Inc. (NYSE: NKE). Nike had a longer runway to be the king of the performance athletic shoe sector. But the company’s fall from grace has been just as noticeable to consumers and investors.

That leads to the biggest problem. Nike has made a concerted effort on a turnaround strategy. But it’s been many years, and there’s not a lot to show for it.

Tariffs Add Another Layer of Pain

Lululemon’s margin pressure is more than a demand story. Supply chain costs are compounding it. The company sources roughly 40% of its manufacturing from Vietnam and 28% of its fabrics from mainland China. These have been two of the hardest-hit regions under the current U.S. tariff regime. Management’s guidance explicitly assumes 30% tariffs on Chinese imports and elevated rates on other sourcing countries.

The company flagged that tariffs and the elimination of the de minimis exemption are expected to hit gross profit by approximately $240 million in fiscal 2025. That headwind carries into 2026, and guidance explicitly excludes any potential IEEPA tariff refunds — meaning upside from trade relief isn’t being counted on.

The Reaction Was Swift and Severe

In many cases, an earnings report shouldn’t be taken at face value. Frequently, analysts find nuances that cause them to take a day or more after earnings to render a verdict.

That wasn’t the case with the LULU earnings report. Nearly 20 analysts weighed in on the day after Lululemon reported. With one exception, analysts either lowered their price target or downgraded LULU. In some cases, they did both. The one exception came from Freedom Capital. However, the upgrade was to a Hold from a rare Strong Sell.

But as bad as that is, that’s not the real story. In the last 12 months, the consensus price target for LULU stock has been cut by over 50%. And many of the new analysts’ price targets are well below the consensus price of $165.13.

The Chart Confirms the Damage

The technical picture offers little comfort. LULU is trading at $114, well below its 50-day moving average of $140.78 — a level that has now flipped into firm resistance after acting as support earlier in the year. The stock has been in a sustained downtrend since peaking near $230 in late 2025, a decline of roughly 50% over the past year.

The RSI tells a conflicted story. The 14-period RSI sits at 27.53, deep in oversold territory — a level that historically precedes at least a short-term bounce. However, the signal-line RSI at 38.35 hasn’t confirmed a reversal, and oversold conditions in a downtrend can persist longer than investors expect. Today’s volume spike on an earnings miss is also a concern — high-volume breakdowns often mark capitulation, but they can also accelerate the move before a floor is found.

For LULU to reclaim technical ground, it would need to close back above the $130 to $135 range and begin compressing the gap with the 50-day moving average. Until then, the path of least resistance remains lower.

How Lululemon Can Make a Comeback

Industry analysts believe the company may get a boost from the GLP-1 movement. Bank of America analysts projected that weight loss from GLP-1s could drive wardrobe revamps, particularly among the affluent, and that athletic apparel brands like Lululemon could benefit from healthier lifestyles.

That opinion was seconded by Bernstein’s apparel analyst, Aneesha Sherman, who noted that a wide swath of retailers could benefit from GLP-1 users refreshing their wardrobes, specifically naming Lululemon.

Industry commentary has noted that specialty retailers like Lululemon are reporting growth in activewear sales as GLP-1 users embrace new fitness goals, while fast-fashion retailers with broader size ranges have seen more uneven results.

Challenges Remain, But Lululemon Can Recover

Lululemon has achieved iconic brand status in a short period of time. That’s a halo that doesn’t lose its shine quickly. However, when wallets tighten, a $100 price tag with a logo on it stops being a status symbol and starts being a target.

But that could change if the economic growth suggested by the May Jobs report begins to spread. The logo still means something. The question is whether management can remind consumers why, before a cheaper alternative becomes the new default.

Leave a Reply