PepsiCo Inc. (NASDAQ: PEP) reported Q1 2026 earnings on April 16. The results were good, but maybe in a better-than-expected way. Nevertheless, PEP stock is up about 2% since the report, and analysts are raising their price targets. That sets the table for Coca-Cola (NYSE: KO), which reports earnings on April 28. Analysts are bullish on KO, and while both companies are solid, blue-chip names, there are reasons why Coca-Cola may be a more profitable short-term trade.

Table of Contents

Better Earnings, But a Similar Theme

Pepsi delivered a double beat with adjusted EPS coming in at $1.61, which beat estimates for $1.55. On the top line, the company delivered revenue of $19.44 billion, beating estimates for $18.89 billion. Analysts have been quick to raise their price targets, with BNP Paribas having the highest target, moving to $195 from $191. However, the consensus price target for PEP stock is still around $170, which is only about a 7.5% increase from its closing price on April 17.

This is where it’s important to note what many investors already know. Pepsi and Coca-Cola are frequently linked together, but the companies are different. Many investors prefer Pepsi for its diversified business model that includes a snacks business in addition to its signature beverage brand.

However, that diversification has come with some margin complexity as the company deals with supply chain concerns, and consumers deal with inflation. The bottom line is that the company’s earnings reports were solid and encouraging. But much of that good news may be priced in, leaving limited room for upside.

Coca-Cola Earnings Are on Deck – Where the Opportunity May Lie

Coca-Cola is scheduled to report Q1 2026 earnings before the market opens on April 28. Analysts are projecting adjusted EPS of 81 cents, which would be an 11% year-over-year increase. Right now, analysts have a consensus Buy rating on KO with a consensus price target of $85, which is almost 12% higher than the closing price on April 17.

But here’s where the opportunity may lie. Analysts have been raising their price targets before earnings. That includes Jefferies and UBS Group, which have price targets of $90, which is over 5% above the consensus target.

That suggests that KO may not have had its catalyst moment yet, and that’s why this may be a time for investors to take a position in the stock.

The One Metric That May Set KO Apart

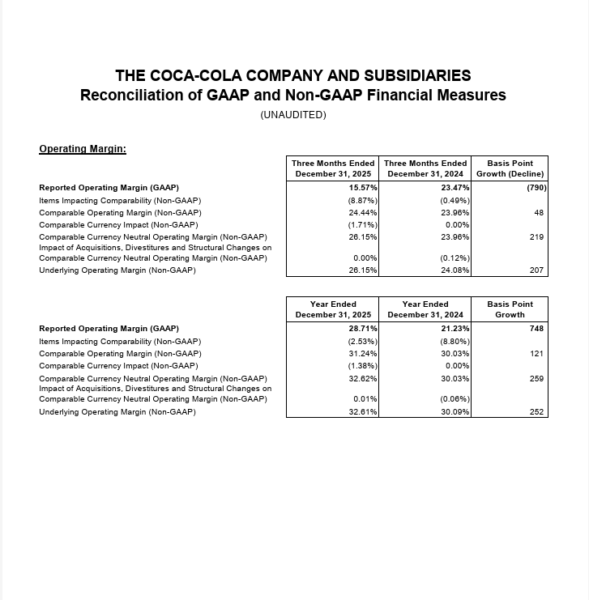

It bears repeating: Pepsi and Coca-Cola are both solid companies. However, when comparing operating margin, there’s a clear bullish case for KO. In this case, Coca-Cola delivered full-year 2025 operating margin of 31.3%. Additionally, operating income rose 5.1% to $15 billion on $47.9 billion in revenue.

By contrast, PepsiCo’s full-year operating income dropped 19.57%, weighed down by $1.9 billion in intangible asset impairments, including the Rockstar energy brand. But why? This comes down to the company’s business models. Coca-Cola’s asset-light, concentrate-and-brand model allows wider margins to absorb input cost shocks, tariffs and FX headwinds when compared to Pepsi’s vertically integrated food-and-beverage operation.

The Dividend: Why Higher Yield Doesn’t Always Mean Better

For income investors, the comparison between KO and PEP gets interesting — and a little counterintuitive. On the surface, PepsiCo looks like the more attractive dividend stock. Its yield of roughly 3.9% is meaningfully higher than Coca-Cola’s approximately 2.9%. And with 53 consecutive years of dividend increases, PEP has earned its Dividend King status.

But yield alone doesn’t tell the whole story. What matters just as much is whether a company can sustain and grow that dividend over time, and that’s where the numbers start to diverge.

Coca-Cola carries a payout ratio of approximately 67%, supported by free cash flow coverage of around 71%. That’s a conservative, well-cushioned profile. PepsiCo, by comparison, pays out roughly 93% of net income in dividends, with free cash flow coverage closer to 63%. When a company is paying out nearly all of its earnings as dividends, there’s very little buffer if business conditions deteriorate.

The concern becomes more concrete when you look at the raw numbers. In fiscal year 2025, PepsiCo generated free cash flow that was nearly identical to the total dividends it paid out — a coverage ratio of essentially 1.0x. There is no margin for error there. One difficult quarter, one unexpected charge, and the math gets uncomfortable.

Coca-Cola, meanwhile, has guided for approximately $12.2 billion in free cash flow for 2026, which puts its dividend on considerably firmer footing going forward. The company has raised its dividend for 64 consecutive years, and the trajectory of its balance sheet suggests that streak is not under pressure.

The bottom line for income investors: PepsiCo’s higher yield is real, but it comes with a tighter rope. Coca-Cola’s lower yield is backed by a more sustainable model — and for long-term dividend investors, sustainability tends to matter more than yield at the point of purchase.

The Short-Term Case for KO

Pulling this together, the argument for Coca-Cola as the better near-term trade rests on a few converging factors. Earnings are still ahead, analyst sentiment is strong and trending higher, the operating margin profile is superior, and the dividend is on a more secure foundation.

PepsiCo had its moment on April 16. The beat was real, the targets moved up, and the stock responded. That’s a good outcome, but it also means the easy money may have already been made for short-term traders. Coca-Cola investors are still waiting for that catalyst.

With KO reporting April 28, a company that has topped Wall Street estimates in each of the last four quarters, the setup looks favorable. The FIFA World Cup partnership and the ongoing Fairlife expansion signal that management is investing in growth, not simply defending legacy brands. And with analysts like UBS and Jefferies carrying $90 price targets well above the current consensus, there is room for the stock to reprice higher if earnings deliver.

Both Are Refreshing, But One May Be More Timely

Neither of these stocks is a bad investment. PepsiCo remains a global powerhouse with a 53-year dividend streak and a diversified business that has real long-term appeal. Investors who own PEP have no compelling reason to sell based on fundamentals.

But for investors evaluating where to put new money to work right now, Coca-Cola presents a timelier opportunity. The stock has more analyst-implied upside, a cleaner margin story, a more sustainable dividend, and an earnings catalyst that hasn’t happened yet. Sometimes the better trade isn’t about finding a broken company to fix; it’s about finding a strong company before its next good news. Right now, that company may be Coca-Cola.

Leave a Reply