The Magnificent 7 is a group of technology stocks that have produced outsized gains for investors. This was due to each company’s market influence in its respective industry. And in 2024 and 2025, artificial intelligence (AI) became a central part of that market influence for many of these companies.

Table of Contents

If investors wanted growth, they simply had to own one or more of these stocks. One of the best ways to do that was through the SPDR S&P 500 ETF Trust (NYSEARCA: SPY), which holds all of these stocks. However, while the SPY has returned over 30% in the last 12 months, you would have likely done better by owning one or more of these individual stocks.

But 2026 is a different story. The Magnificent 7 stocks have become the Seven Dwarfs, with the “best performers” down just over 4% as of the market close on April 6. However, while valuation is a concern for each of these stocks, it takes a bit longer to identify a structural problem that explains the negative sentiment.

In many cases, the stocks have been a victim of their own success. This is where investors can find liquidity when they need to raise capital for life events like taxes or simply to take advantage of sector rotation opportunities.

As another earnings season gets ready to start, it’s a good time to consider which of these stocks may deserve a look in your portfolio, and which ones may be better to avoid. It’s a topic that would make a great bar debate, so here are my best and worst Magnificent 7 stocks fo Q2 earnings season.

Best Magnificent 7 Stock: Microsoft – The Comeback Kid That Is Massively Oversold

If you’re looking for a stock where the punishment clearly doesn’t fit the crime, Microsoft (NASDAQ: MSFT) is it. Shares plunged roughly 23% in the first quarter of 2026 — the company’s worst quarterly performance since the 2008 financial crisis — and yet the actual business has rarely looked better. Revenue grew 17% year-over-year to $81.3 billion in its most recent quarter, operating income rose 21%, and Microsoft Cloud crossed $50 billion in a single quarter for the first time. That’s not a company in distress. It’s a company being punished for spending aggressively on a future that hasn’t fully arrived yet.

The core concern on Wall Street is straightforward: Microsoft’s capital expenditures surged 66% year over year to $37.5 billion last quarter as the company continues to invest in AI data centers, GPUs, and cloud infrastructure. Azure growth, while still a robust 39%, decelerated slightly from the prior quarter. And in an environment where investors are already jittery about AI’s return on investment, that combination was enough to trigger selling.

But the selloff has created a compelling setup heading into earnings, expected in late April. Microsoft’s 14-day RSI recently fell below 30, deep into oversold territory, even as analysts maintain an average price target near $590 — a massive premium to where the stock has been trading. The valuation multiple hasn’t been this compressed since the fourth quarter of 2022. That was when OpenAI introduced ChatGPT, and before Microsoft’s AI-driven re-rating began, which feels like a meaningful marker.

The bull case is straightforward. Commercial remaining performance obligations — essentially the company’s forward revenue backlog — more than doubled year over year to $625 billion, a staggering figure that signals customers are locking in multi-year AI and cloud commitments. Demand for Azure continues to outstrip supply; CFO Amy Hood has said growth could have been even higher if the company had directed more chip capacity toward cloud customers. Microsoft returned $12.7 billion to shareholders through dividends and buybacks last quarter, up 32% from a year earlier. These are not the metrics of a company losing the AI race.

Will Q3 earnings be a flawless beat? Probably not — cloud growth is still moderating, and capacity constraints will linger. But MSFT at these levels already prices in a lot of bad news. Investors willing to look past one or two quarters of noise could be getting one of the great AI infrastructure businesses in the world at a historically attractive price. Sometimes the best trade is the one that feels the most uncomfortable.

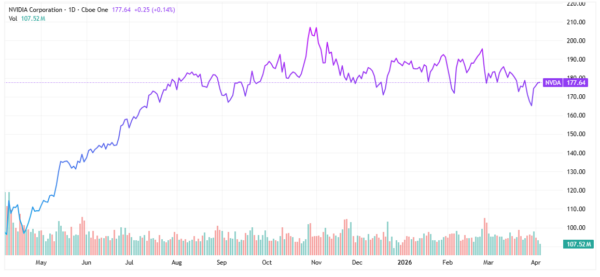

Honorable Mention: NVIDIA – Still the King, But Know What You’re Buying

It’s almost impossible to write about AI stocks without giving NVIDIA (NASDAQ: NVDA) its proper due. Fiscal year 2026 revenue came in at roughly $216 billion — up 65% year-over-year — and the company guided for $78 billion in Q1 fiscal 2027 revenue. These are numbers that most technology companies can only dream about.

But there’s a wrinkle that investors need to understand before earnings season: NVIDIA has no China data center revenue baked into its near-term guidance. Export control restrictions removed NVIDIA’s H20 chips from the Chinese market, costing the company billions in revenue and forcing a painful write-down last year. Whether that headwind gets resolved (or gets worse, depending on tariff developments) is one of the biggest single variables for the stock.

NVIDIA deserves its place on any serious investor’s watchlist. The Blackwell chip architecture is ramping, hyperscaler spending on AI infrastructure remains ferocious, and demand is structurally supply-constrained. But the stock has already recovered significantly from its lows, and the China overhang means Q1 results could disappoint relative to loftier expectations. NVDA is a long-term hold, not necessarily a short-term trade. For patient investors, it remains the backbone of the AI infrastructure build-out.

Worst Magnificent 7 Stock: Meta Platforms – Litigation Will Keep Gains in Check

Meta Platforms (NASDAQ: META) is a genuinely difficult stock to argue against on fundamentals. The advertising engine is humming, AI is improving ad targeting, Reels has kept users engaged, and the FTC’s antitrust case, which threatened to force the company to divest Instagram and WhatsApp, ended in a decisive victory when Judge James Boasberg ruled in November 2025 that Meta does not hold a monopoly in social media. Mark Zuckerberg can be forgiven for exhaling.

The problem is that one legal door closing has opened a dozen others, and the ones that just swung wide are far messier. In late March 2026, a New Mexico jury ordered Meta to pay $375 million after finding the company misled users about platform safety and failed to protect children from predators. A day later in Los Angeles, a separate jury found Meta negligent in a personal injury trial involving social media’s mental health effects on young users. That California case is explicitly tied to roughly 2,000 additional pending lawsuits. It’s a bellwether, and the bellwether did not ring in Meta’s favor.

These aren’t isolated incidents. More than 40 state attorneys general have active lawsuits against Meta related to child safety. The New Mexico attorney general has publicly stated that these verdicts could prompt Congress to revisit or revamp Section 230 of the Communications Decency Act — the liability shield that has protected platforms for 30 years. If that shield gets meaningfully weakened, it doesn’t just affect one quarter’s earnings. It changes the fundamental cost structure of the business.

Then there’s the spending side. Meta has guided for up to $135 billion in AI-related capital expenditure in 2026 — a staggering sum that, combined with Reality Labs’ $80-plus billion in cumulative operating losses since 2021, means the company is writing enormous checks in multiple directions simultaneously. The stock recently traded near $595, well off its 52-week high of $796. That’s meaningful compression, but it doesn’t necessarily make Meta cheap when you factor in a legal liability that is growing, not shrinking.

Wall Street still overwhelmingly rates META a buy, and it’s easy to see why — the core ad business is exceptional. But heading into earnings, the headline risk from litigation is real, and the FTC appeal (now before a higher court) keeps that antitrust cloud partially overhead. The stock can absolutely work over the long run. But for the near-term window around earnings, there are cleaner bets in the group.

Conclusion

Earnings season has a way of forcing clarity on stories that otherwise drag on for quarters. For the Magnificent 7 in 2026, the tension isn’t about whether these businesses are great — most of them are — it’s about whether the prices reflect the complications that come with being dominant at scale.

As always, these aren’t buy or sell recommendations — just one investor’s read on where the risk-reward sits as earnings season kicks off. The bar debate version is a lot more fun with a cold drink in hand.

Leave a Reply