Keep an eye on NVIDIA Corp. (NASDAQ: NVDA). We were hoping to see an explosive surge in NVDA stock – especially with its better-than-expected numbers. Revenue hit $68.13 billion, which was well ahead of expectations of $66.21 billion. EPS of $1.62 beat by eight cents. It also saw record quarterly data center revenue of $62.3 billion, up 75% year over year. NVIDIA even declared a one-cent per share dividend, which is payable on April 1 to shareholders of record as of March 11.

Table of Contents

Moving forward, the company said it expects to see revenue of $78 billion, plus/minus 2%, which is also well above estimates of $72.8 billion.

Yet, the market reaction wasn’t as great as expected, which shocked analysts.

For example, as noted by Seeking Alpha, “Morgan Stanley analyst Joseph Moore… was ‘surprised’ by the muted reaction to the stock, given that the results were the ‘largest, cleanest beat and raise in the history of the semis industry.’”

AI Capex Spending Concerns Are Weighing on the Stock

One reason we’re not seeing a stronger response is that markets are still concerned about high levels of AI capex spending, which, according to JPMorgan, is based on faulty logic.

On one side of the argument, there’s fear that AI will disrupt the entire software industry. Second, there are concerns that hyperscalers are spending too much on AI capex and that these large investments won’t pay off going forward. But both can’t be true, say the analysts.

“If AI companies are going to disrupt, destroy, and replace all software companies, those AI stocks should be more valuable. Or if AI is overvalued and those big capital expenditures are never going to pay off, software stock investors should be less worried about their companies getting wrecked by AI,” as quoted by Yahoo Finance.

In addition, according to Dan Hanbury, global strategic equity co-portfolio manager at Ninety-One, as quoted by CNBC, “What is weighing heavily on investors’ minds is how NVIDIA can maintain its phenomenal growth rate now its core customers — the hyperscalers — are mostly depleting their cash flows, spending on AI-related capex.”

Before you dismiss these arguments as analysts talking their book, consider what NVIDIA said in its earnings report. That is, enterprise customers are using agentic AI at an explosive rate. So when hyperscalers talk about insatiable demand, it’s because they have that demand on their books, and it’s only going to increase.

NVIDIA Is Still a Top Pick

According to analysts at Bank of America, NVDA stock is still a top pick. The firm also reiterated its buy on the tech giant with a price target of $300.

“Our positive view on NVIDIA is based on its underappreciated transformation from a traditional PC graphics chip vendor into a supplier of high-end gaming, enterprise graphics, cloud, accelerated computing, and automotive markets,” they added.

The consensus price target for NVDA stock is $265.14. That’s 41% upside from its closing price on Feb. 26.

What Should Investors Take Away From NVDA Earnings?

In short, the quarter was exceptional. The guidance was strong. The fundamentals remain powerful. And NVDA stock should reverse course. But investor psychology is a funny thing, and nobody can say for sure when that reversal will happen.

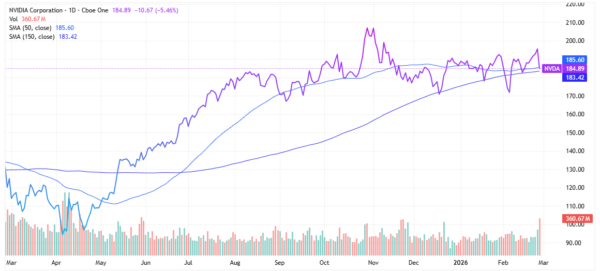

The stock is trading near both its 50-day and 150-day simple moving average (SMA). That could be a key inflection point. Meaning investors should wait for confirmation of a move above or below these levels before deciding on your next move.

However, at some point, NVIDIA stock is likely to move higher. The market’s hesitation isn’t about what NVIDIA did — it’s about whether this level of AI-driven demand can persist. For long-term investors who believe AI infrastructure spending is still in its early innings, NVIDIA remains one of the highest-quality names in the space.

Leave a Reply