While a compelling case can be me for the open market, those daring to trade in the options arena must embrace a probabilistic ontology. Case in point is semiconductor firm Marvell Technology (NASDAQ:MRVL). One of the more crucial enterprises for artificial intelligence, Marvell provides essential data infrastructure. Basically, it represents the nervous system for machine learning protocols through high-speed networking, storage and custom chips.

Table of Contents

Based purely on narrative, you would expect MRVL stock to perform well — and it occasionally demonstrates patches of robust upswing. However, on a broader level, MRVL hasn’t exactly been the paragon of consistency. Since the start of the year, the security is down 24%. Over the past five years, it’s up 77%, albeit with severe peaks and valleys.

While tech names tend to be non-ergodic, MRVL stock seems to relish taking the description to new heights. Still, for options-focused speculators, Marvell’s volatility isn’t a bug — it’s a feature.

In other words, any effort to trade MRVL stock on valuation metrics is incredibly problematic as this approach leads to what I term “ought-to” logic. For example, many investors are tempted to cite Marvell’s financial strengths and present a case of undervaluation, ultimately leading to a rerating.

Unfortunately, such thinking — while no doubt carried out with good intentions — begs the question as it smuggles the conclusion (that MRVL will rerate higher) into the premise (that Marvell is undervalued). What should actually take place is that the speculator allows the data to speak for itself.

When you do that, you can build an empirical case — and ultimately have more confidence in your trading decisions.

Using Data Science to Reveal the Structure of Risk

One of the first mistakes that traders make is to rely on time-based chronological frameworks. It’s easy to do because, as humans, viewing narratives chronologically comes organically and naturally. There’s a reason why most movies feature a linear progression. While non-linear films like “Memento” add intriguing flavor, they’re also difficult for the average audience to follow.

To be sure, there’s a simple elegance to a methodology like technical analysis. An expert identifies a credible behavioral pattern on the chart, plots a reasonable forecast and allows you, the reader, to decide whether to place the wager or not.

Here’s a harsh reality check: the financial market is one of the most complex environments known to man. It is reflexive, reactive and heteroskedastic, among many other characteristics. What’s worse, exogenous factors can enter the system at any moment and wreak absolute havoc. Therefore, it beggars disbelief that mathematically untrained pundits drawing lines on charts can consistently deliver useful insights.

Rather than thinking chronologically, it’s vital that we think hierarchically.

Imagine that you took a single 10-week strand of pricing data of MRVL stock. Obviously, the return during this period won’t tell you much about the probabilistic performance of the other weeks in the dataset. But let’s say you took hundreds of rolling 10-week sequences of MRVL and stacked them together in a fixed-time distribution. Suddenly, the chart that you plot would reveal the underlying probabilistic structure.

Essentially, one-off events — whether unusually strong or weak — will not be weighted enough to affect the overall distribution due to a lack of frequency volume. However, events that happen consistently and recurringly will feature the greatest representation. These data points will create bulges in probability mass.

Stated differently, the bulges symbolize risk geometry. Essentially, under multiple trials, a public security will reveal its inherent tendencies. As such, calculating risk geometry doesn’t just tell us where a security may go — it also tells us where it stops going.

For options traders, this transitional probability is the more useful insight.

Identifying a Potentially Lucrative Trade for MRVL Stock

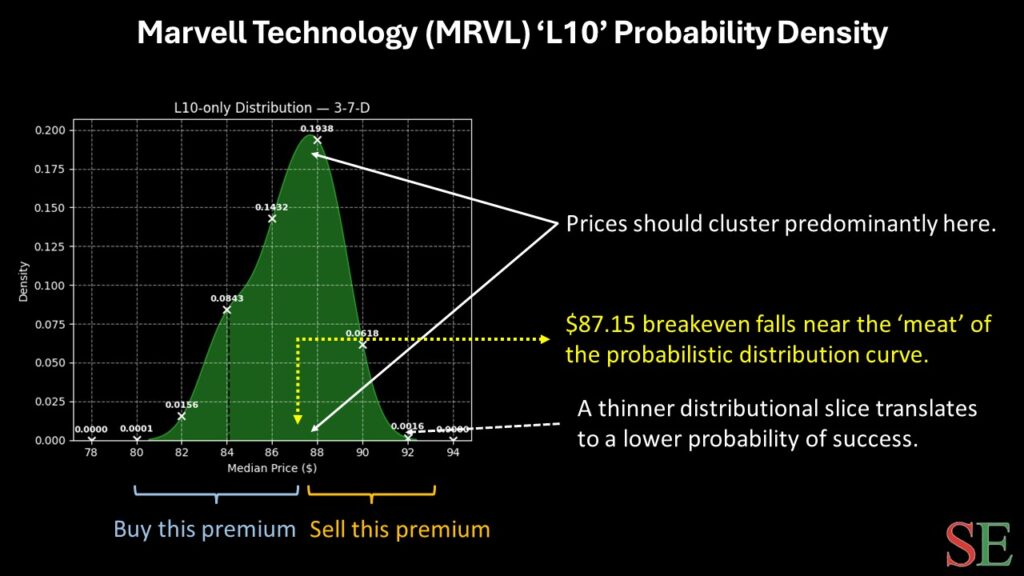

Using the price history of MRVL stock going back to January 2019, its forward 10-week distribution would likely see outcomes range between $82 and $91 (assuming an anchor price of $84.09, Friday’s close). Further, price clustering would likely be predominant at around $89, thus indicating a bullish bias.

However, we’re interested in the typical response to the current quantitative signal, which is the 3-7-D sequence; that is, in the past 10 weeks, MRVL stock printed only three up weeks, leading to an overall downward slope.

Under this setup, the forward 10-week returns would likely range between $80.50 and $92, with price clustering likely to occur near $88. To be fair, that doesn’t give us much variance relative to price clustering dynamics under aggregate or baseline conditions. As such, you might be tempted to consider a more conservative options strategy, such as the 80/85 bull call spread expiring Feb. 20, 2026.

Here’s the problem with that trade in particular. If MRVL stock rises through the second-leg strike ($85) at expiration, the maximum payout is only about 59%. I believe we may be at risk of leaving money on the table with this spread, considering that it’s a capped-risk, capped-reward transaction.

A better idea (in my humble opinion) is the 85/90 bull spread, also expiring Feb. 20. To be sure, it’s a much more aggressive wager as MRVL stock must rise through the $90 strike to trigger the maximum reward. However, the capped payout stands at roughly 133%, which is a much more palatable proposition.

Plus, with a breakeven price of $87.15, this threshold is sitting atop the peak of probability density for the 3-7-D sequence. In other words, there’s a solid chance of breaking even — while the width of the second leg allows you to stretch for potentially robust rewards.

Finally, the big selling point is probability decay. Between $88 and $90, probability density drops by 68.11%, which is steep. However, from $86 to $88, probability density actually rises by 35.34%. You don’t want to cap your reward when the underlying probability mass is rising as that would mean you would have a greater chance of absorbing an opportunity cost.

Instead, the 85/90 spread arguably gives you an ideal balance between profit maximization and opportunity cost limitation.

Leave a Reply