When looking at Petco (NASDAQ: WOOF) from the outside, it’s difficult not to see the potential for a comeback. After all, Americans love their pets — it’s one of the truly unifying characteristics of this nation a deeply fractured ideological divide. However, investors simply do not love WOOF stock.

Table of Contents

Since the start of the year, Petco has already lost more than 15% of its value. Over the past five years, WOOF stock plunged roughly 90%. Just when you think a technical floor has been secured, that the equity couldn’t possibly fall any further, WOOF ends up proving you wrong. As such, I’m not terribly confident ahead of the company’s fourth-quarter earnings report.

By the print, Wall Street analysts are looking for earnings per share of 1 cent on revenue of $1.51 billion. In the year-ago quarter, Petco posted a loss per share of 5 cents on revenue of $1.55 billion, missing on both the top and bottom lines. What’s going to bother a lot of experts is the erosion in the headline growth number, especially amid a weakening consumer economy and rising competition.

Still, there will be plenty of speculators who will look at WOOF stock as an extreme value play, especially with a subterranean price-to-sales multiple of 0.11 and a forward earnings multiple of less than 8. Despite the tempting offer, though, the smart money remains unconvinced.

Volatility Skew Reveals the Smart Money’s Posture Toward WOOF Stock

While Petco stock may appear to be cheap, that term can be a tricky one. What we don’t want is for a cheap security to become even cheaper after we buy it. However, that’s the concern that’s being signaled by the smart money, at least according to the volatility skew.

Definitionally, the volatility skew is a screener that identifies implied volatility (IV) — or a stock’s potential range of motion — across the strike price spectrum of a given options chain. Basically, the tool showcases the surface-area distortion of volatility space, allowing retail traders to better understand how the smart money is structuring its risk profile.

In the case of the next upcoming weekly options chain (expiring March 13), the skew is relatively flat around the spot price. This profile suggests a lack of urgency in mitigating directional risk. Where there is a curvature spike occurs at the edges (specifically the left-hand side). Here, the structuring points to mitigation against tail risk.

Also, you’ll notice that the skew toward the right-hand side (toward higher strikes) is relatively muted. Essentially, smart money traders are refusing to position for upside convexity. In the case of the March 13 expiration date, the philosophy is making sure you don’t lose the game rather than running up the score.

It’s a similar situation (but on a greater scale) for options chains further down the line, such as the April 17 (monthly) expiration date. Here, put IV on the left-hand side soars to about 436%, whereas call IV on the right-hand side peaks at 212.2%. Again, the priority is to ensure against tail risk rather than to seek upside convexity.

For me, this risk structuring represents a major warning. We’re talking about a really cheap stock here (being last priced at $2.38 a pop). Even with the potential to make gobs of money on the contrarian side of the trade, the smart money is still firmly in a defensive shell.

Quantitative Picture Fills in the Rest of the Gap for Petco Stock

Enumerative induction, or the use of past analogs to help frame a probabilistic path forward, has its limitations. It’s a form of pattern recognition. If you happen to be on a hot streak, you might be tempted to continue betting on this streak. However, it’s important to realize that the future is not necessarily compelled by the past.

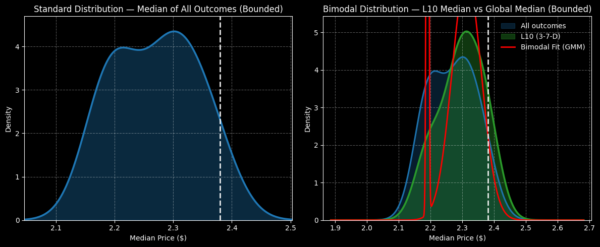

That being said, enumerative induction is probably the best mechanism for understanding the trading tendencies of public securities. Regarding Petco stock, the main concern about betting on the underlying company’s upcoming Q4 earnings report is the security’s negative bias. Using enumerative induction, we can calculate that WOOF’s median 10-week return would land between approximately $2 and $2.50, with probability density peaking at around $2.30.

The problem? As I mentioned earlier, the last closing price of WOOF stock was $2.38. Statistically speaking, then, if you were to hold WOOF for a period of about two months, you’d be looking at a loss most of the time of about 3.4%.

Given the poor exceedance ratio (how likely it would be for WOOF stock to rise above spot), you would only be expected to be profitable about one-third of the time betting on WOOF at scale.

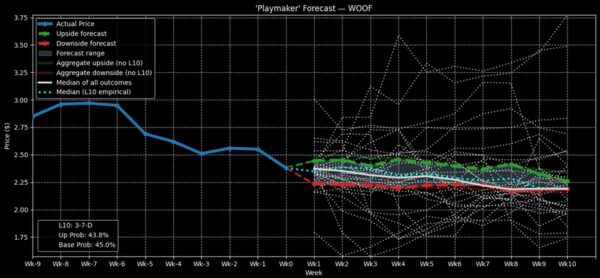

Now, the bullish argument from the quantitative side is that we’re not just approaching Petco stock randomly. Instead, in the last 10 weeks, WOOF printed only three up weeks, leading to an overall downward slope. Given that there’s so much bearishness baked into this market structure, surely the bulls will help move the stock higher?

Technically, the answer is yes, it does. However, we’re talking about minuscule changes. Essentially, the forward distribution under 3-7-D conditions would allow WOOF stock to reach around $2.53 under the best of circumstances. The downside risk would still remain around $2 (or slightly worse).

Over the full breadth of the next 10 weeks, the exceedance ratio between the baseline and conditional frameworks is little changed. That’s why the smart money isn’t gung-ho on WOOF stock. It sees Petco as a value trap, and it’s really hard to argue against it.

Rationality Trumps Narratives

I’m a really big proponent of the pet care market overall. Again, Americans love their furry friends, and that’s not going to change anytime soon. I also previously liked the idea of WOOF stock being a value play. However, that was before the complete meltdown of this security.

I’m just afraid that there’s not much growth here. Whether you look at this trade fundamentally, technically or quantitatively, the picture continues to look poor. As such, I would consider something like a straight put option, such as the $2 put expiring Jan. 15, 2027.

Otherwise, I regrettably believe Petco is a case of good money chasing after bad.

Leave a Reply