I don’t want to sound too alarmist, but a massive warning sign just flashed for the SPDR S&P 500 ETF Trust (NYSEARCA: SPY) that may have serious implications for membership-only retailer Costco (NASDAQ: COST). One of the hallmarks of suburban economic power, Costco is about to release its second-quarter earnings report. But after a strong start to the new year, COST stock appears to be running on fumes.

Table of Contents

At first glance, circumstances seem normal. For the upcoming disclosure, scheduled for release on Thursday after the closing bell, Wall Street analysts expect earnings per share of $4.54 on revenue of $69.26 billion. In the year-ago quarter, Costco posted EPS of $4.02 on revenue of $63.72 billion, a performance that missed slightly on the bottom line but exceeded on the top.

Generally, while Costco’s financial print can be hit-or-miss, market sentiment for COST stock tends to be positive. For example, over the past five years, the security has gained roughly 218%. Over the past year and a half, COST has carried an earnings multiple of over 50.

Basically, such a ratio translates to an earnings yield of around 2%, which some might argue is alarmingly low. After all, you could just put your money into risk-free Treasuries and get double the aforementioned yield.

As it turns out, some investors appear to be getting the message. In the past year, COST stock is down about 4%. With the U.S. and Israel launching a military strike against Iran, the disruption that this conflict poses for the global economy forces a rethink for previously high-powered names.

Volatility Skew Reveals a Cautious Outlook for COST Stock

As I’ve pointed out previously, volatility skew is one of the most important indicators to watch. Definitionally, the skew identifies implied volatility (IV) — or a stock’s potential range of motion — across the strike price spectrum of a given options chain. Essentially, it’s a screener that showcases the surface-area distortion of volatility space, allowing traders to identify how the smart money is positioning risk.

If we were to frame the skew as a security protocol, it would reveal the vulnerability points that are most at risk. Therefore, the entity seeking protection would beef up defenses to address said vulnerabilities. This beefing up leads to elevated put IV at the strike prices of concern.

What’s fascinating is that, for the April 17 expiration date, the skew shows put IV rising on both ends of the strike boundaries. With the rising skew toward the left-hand boundaries (toward lower strikes), this setup suggests that smart money traders are concerned about downside tail risk. Toward the right, the priority appears to be protecting actual long exposure to COST stock via synthetic shorts.

Notice what’s happening with call IV. Relative to puts, there’s little urgency to seek upside convexity. Again, the priority among sophisticated market participants appears to focus on not losing money rather than efforts toward extracting capital growth.

We see a similar skew for the March 6 weekly options chain, the expiration date closest to Costco’s Q2 disclosure. The bulk of curvature rise is concentrated on the far-left side of the spectrum. Again, the main motif here is that traders are focused on mitigating a sharp loss rather than betting on a rising share price.

The Warning Signal for Costco Stock and the Broader Index

According to the Black-Scholes-derived expected move calculator, Costco stock for the April 17 expiration date is expected to land between $933.68 and $1,081.34. However, this assumption is based on a static formula that does not account for prior market context. Essentially, it’s a reference marker — one that’s only valid if we assume a world that simply may not exist.

One of my biggest contentions about Black-Scholes is that the market generally operates under the Markov property; that is, forward probabilities depend on the context in which the calculations are being applied. For example, in a football game, the odds of winning the contest will change depending on whether you have a sizable lead or not.

My problem with relying exclusively on Black-Scholes to make forward estimations is that the formula is completely blind to context. So, whether COST stock has just completed a massive rally or recovered from a catastrophic fall, the same math is applied. Context is merely the starting point of a predefined analysis and offers no fundamental change to the estimated distribution.

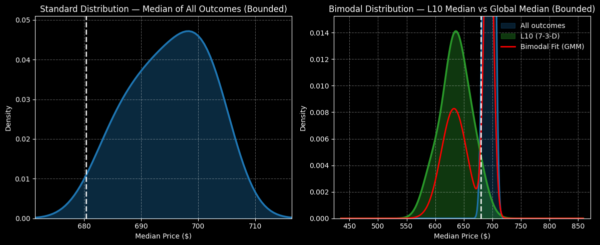

Rather than this parametric (predefined) approach, Markov systems measure and account for the distributional changes that can occur due to different contexts. In the case of the broader equities market, the SPY ETF in the past 10 weeks printed seven up weeks. However, the overall slope of this 10-week trend has been negative.

What’s so special about this 7-3-D sequence? It’s an extremely rare quantitative signal, for one. More critically, when this signal flashes, past analogs suggest that the future weeks could lead to sharply negative price action before an eventual slow recovery.

Now, it must be said that all future statements are inductive by nature; there’s nothing that logically compels the 7-3-D sequence to cause a downturn in the SPY ETF. However, my argument is that this unique harbinger is flashing at a particularly vulnerable time for the U.S.

Also, it’s worth keeping in mind that if the Iranians manage to drag the U.S. into a war of attrition, the geographic advantage (Iran being an extremely mountainous country) may lean to them. That’s another reason why I don’t view this signal as merely an inductive fantasy.

Where Does This Leave the Retailing Giant?

Turning our attention back to COST stock, the concern in the weeks ahead is that traders may be tempted to trim their exposure to the retailing giant. With a year-to-date performance of nearly 17% along with a hot earnings multiple, I’m not entirely sure if I trust the rally to continue.

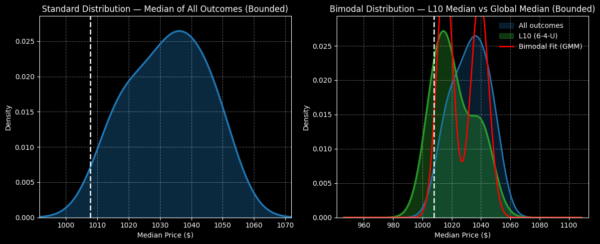

Further, COST’s quant signal — a 6-4-U sequence over the past 10 weeks — doesn’t lend itself to a particularly strong forward performance. Over the next 10 weeks, an inductive calculation predicts a range between $980 and $1,065. The problem, though, is that on an aggregate basis, the forward 10-week return would typically range between $990 and $1,070.

I’m not sure if I like the idea of paying a long premium for a quant signal with a lower-than-average probabilistic profile. For those who want to aggressively speculate, a near-term wager featuring the 985/980 bear put spread expiring March 6 could be enticing. Otherwise, COST stock might be a name to watch on the sidelines.

Leave a Reply