Valuation is a common theme in the mainstream financial press. Many analysts would say, therefore, that this is a time to avoid high P/E stocks. That is, stocks with a high price-to-earnings (P/E) ratio. The P/E ratio measures how much you pay for every one dollar of a company’s future earnings. Lower is better.

Table of Contents

But what’s considered a high P/E ratio? That’s a relative term. A standard measure is to look at the average P/E ratio of all the stocks in the S&P 500, which as of the market close on March 6, 2026, was 27.4x.

For investors of a certain age, having an average P/E around 27 would seem absurd. Just 30 years ago, a P/E above 10 was considered high-risk. And that’s why many stocks are deemed expensive.

That said, many of these high P/E stocks have continued to defy gravity. And that’s due to something that every investor needs to focus on, which is growth. Many of these companies, such as NVIDIA Corp. (NASDAQ: NVDA) have been growing at exceptional rates that make investors eager to bid up their respective stocks.

You also need to consider that many stocks are expensive to the S&P 500 but may not be expensive compared to their market sector. For example, technology companies, in general, will have higher P/E ratios compared to utility companies because they provide outsized growth.

This creates a clash of philosophies for investors. On the one hand, stocks don’t move in the same direction forever. Many stocks are down sharply in 2026 due to profit-taking and sector rotation. At the same time, time in the market is more important than timing the market. Investors take a risk by moving out of a high P/E stock that still has upside potential.

Here are three high P/E stocks that fit that criteria. They’re expensive but have a long runway to grow into their valuations.

High P/E Stock to Buy: Palantir Technologies

Palantir Technologies (NASDAQ: PLTR) is as polarizing as it is expensive. Many investors won’t touch the stock because of its contracts with the federal government, and specifically the U.S. Department of War. Other investors will point to PLTR’s high P/E of around 241x as of this writing.

Let’s put that into perspective. In the introduction, I said that technology stocks frequently have sector averages higher than the S&P 500. Palantir is in the software sector, where the average P/E is around 41x. That still makes Palantir very expensive.

However, both of these arguments fail to capture the reasons to own PLTR stock. To begin with, as of the company’s most recent earnings report, Palantir generates about 44% of its revenue from commercial customers. This covers sectors ranging from healthcare to consumer staples to energy.

Second, traditional P/E ratios can be a misleading valuation metric for software companies with high reinvestment rates. This is because GAAP earnings are reduced by heavy spending on R&D and sales. These are investments that drive future growth rather than represent true economic losses. Therefore, P/E can make a profitable, compounding business look expensive on paper.

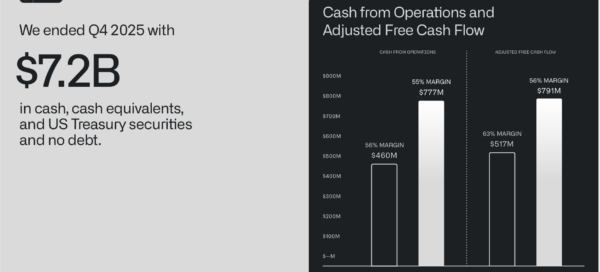

For Palantir specifically, stock-based compensation further distorts GAAP earnings, making the P/E ratio an especially poor standalone metric. Investors may find it more useful to focus on free cash flow, which strips out some of these distortions and better reflects the business’s cash-generating power. On that basis, Palantir has shown accelerating FCF growth alongside a debt-free balance sheet, which suggests underlying business health even when headline earnings metrics appear stretched.

High P/E Stock to Buy: Eli Lilly

Another way to determine if a high P/E stock is worth chasing is the company’s position within its sector. That’s a solid rationale for owning Eli Lilly & Co. (NYSE: LLY). LLY stock is up about 14% in the 12 months ending March 6. However, the stock’s momentum has stalled in 2026. Valuation isn’t the only reason, but it’s one of them.

That said, Eli Lilly is the undisputed leader in the GLP-1 weight loss category. That’s a sector that’s expected to have many years and multiple billions of dollars of growth potential. There’s room for more than one company in this space. But Lilly has an entrenched position that will be difficult to replace.

Plus, Lilly isn’t just about GLP-1 drugs. The company has a long history of expertise in Alzheimer’s disease, oncology, cardiovascular disease, and immunology. It’s also one of the companies that is aggressively pursuing treatments for Alzheimer’s disease. That’s reflected in the company’s expansive pipeline that includes 36 candidates in Phase 3 trials.

High P/E Stock to Buy: Walmart

Walmart (NASDAQ: WMT) is another high P/E stock for investors to consider. For one thing, the company recently switched its listing from the New York Stock Exchange (NYSE) to the NASDAQ to better reflect its ongoing investment in technology in areas like robotics and artificial intelligence (AI).

The retailer is an example of a company that’s not resting on its laurels. Rather than conceding an inch of ground to Amazon (NASDAQ: AMZN), Walmart has aggressively taken the fight to them with its Walmart+ program that has been integral to the company’s post-2020 growth.

Plus, Walmart split its stock in January 2025 to make it more accessible for its employees and other retail investors. Year-over-year (YOY) growth has started to accelerate in the last two quarters of its 2026 fiscal year, which reinforces management’s commentary that the company is capturing a higher share of wallet from higher-income consumers who are shopping at Walmart for discretionary items even as lower-income consumers stick to staples.

All of this reinforces the company’s rock-solid balance sheet that allows it to buy back shares and continue to increase its dividend. In fact, Walmart is a Dividend King, having increased its dividend in each of the last 53 consecutive years.

When You Buy the Best, the Rules Can Be Flexible

High P/E stocks are not for every investor, and the valuation risk is real. But Palantir, Eli Lilly, and Walmart each represent companies with durable competitive advantages and credible paths to growing into their current valuations.

Palantir’s FCF growth and AI-driven expansion, Lilly’s dominance in GLP-1 and a deep clinical pipeline, and Walmart’s relentless operational reinvention make these more than just expensive tickers. For investors with a long time horizon and the conviction to hold through volatility, these stocks offer something increasingly rare in today’s market: genuine upside with a fundamental story to back it up.

Leave a Reply