AST SpaceMobile (NASDAQ: ASTS) dropped its Q4 2025 earnings report on March 2, 2026, and the reaction from Wall Street was… complicated. The stock surged nearly 10% on the day, closing at $86.92 on heavy volume of 13.5 million shares. But here’s the thing — even after that pop, the stock was still trading well above where most analysts think it should be. Sound familiar? If it reminds you of Palantir Technologies (NASDAQ: PLTR) in its pre-profitability days, you’re not alone.

Table of Contents

“Yeah, But” Stock Phenomenon

ASTS has become what traders increasingly call a “yeah, but” stock. The company is checking off a remarkable number of boxes — and yet, analysts keep pumping the brakes.

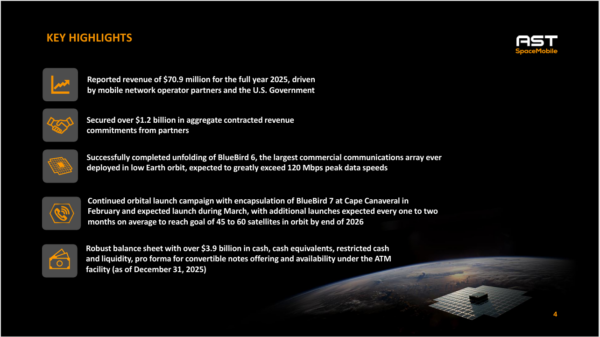

Yeah, ASTS reported $70.9 million in full-year 2025 revenue, driven by mobile network operator partners and U.S. Government contracts. But the company is still deeply unprofitable, burning through cash as it races to get its BlueBird satellite constellation into orbit.

Yeah, ASTS secured over $1.2 billion in aggregate contracted revenue commitments from commercial partners. But the stock, hovering near $87 at Monday’s close, is trading well above most analyst targets. According to data from multiple sources, the consensus price target ranges from roughly $60 to $91. In every case, it implies either modest upside or meaningful downside from current levels. Out of 11 Wall Street analysts covering the stock, the breakdown runs 3 Buy, 5 Hold, and 2 Sell ratings, with a median price target of $80.50.

Yeah, BlueBird 6 — the largest commercial communications array ever deployed in low Earth orbit — successfully unfolded in February, and the company expects its next satellite, BlueBird 7, to launch during March. But profitability remains a distant target, with analysts projecting continued losses through at least 2026.

This Is Exactly Where Palantir Was

Students of recent market history will recognize this setup. Palantir spent years as one of Wall Street’s most controversial stocks. The stock was, and is, perpetually “overvalued” by traditional metrics. It also was, and is, persistently defended by a loyal base of retail and institutional believers, and repeatedly dismissed by analysts waiting for proof of profitability.

The Palantir story eventually vindicated the believers. Once PLTR turned the corner on GAAP profitability, the stock didn’t just drift higher; it launched. By early 2026, Palantir reported its 13th consecutive quarter of GAAP profitability, with full-year 2025 revenue reaching $4.475 billion and net income of approximately $1.8 billion. Palantir’s institutional ownership clearly tells the story of a sentiment shift: it rose from 35% in 2023 to over 60% in early 2026, as the “wait for profitability” crowd finally capitulated and piled in.

The parallel to ASTS is hard to ignore. Like Palantir in its early years, AST SpaceMobile has a technology that genuinely works, a growing list of blue-chip partnerships, and a narrative that captures the imagination. And, like Palantir, analysts are essentially telling investors: “We’ll believe it when we see profitable numbers.”

Where the Stories Diverge — And Why It Matters

But here’s where the ASTS-Palantir comparison gets interesting. There’s one significant way in which AST SpaceMobile appears to be ahead of where Palantir was at a comparable stage: institutional ownership.

ASTS is currently owned by approximately 36.87% of institutional shareholders, 42.25% by insiders, and 20.88% by retail investors. Major players like BlackRock and Vanguard have already taken meaningful positions. This level of institutional conviction — well before profitability — suggests the “smart money” has already done the math and decided the risk is worth taking. With Palantir, institutional ownership lagged for years while retail holders carried the water. Institutions only piled in once profitability was established. ASTS may be compressing that timeline.

Hedge fund ownership has also been building, with 33 hedge fund portfolios holding ASTS at the end of Q4 2025, up from 25 in the previous quarter. That’s not the kind of number you see in a stock where the institutional community is simply waiting on the sidelines.

What the Q4 Report Actually Said

Stepping back to the fundamentals: the Q4 report was genuinely mixed, with revenue being the strongest component. The $70.9 million full-year 2025 figure was driven by product equipment revenue from delivering 15 commercial gateways across five continents, plus service revenue from multiple U.S. Government contracts. The company expects revenue to continue growing in 2026 ahead of commercial service activation.

On the cost side, adjusted operating expenses climbed from $67.7 million in Q3 to $95.7 million in Q4 — a meaningful jump driven by cost of revenues as the company begins actually delivering product at scale. Capital expenditures surged to $406.7 million in Q4 from $258.9 million in Q3, reflecting the aggressive satellite manufacturing buildout. The company added a fourth production site in Midland, Texas, bringing its total manufacturing square footage globally to exceed 500,000.

The liquidity position is genuinely robust. ASTS ended the year with over $3.9 billion in cash, equivalents, restricted cash and liquidity, pro forma for its convertible notes offering and ATM facility availability. That’s a meaningful runway for a company still several years from scaled profitability.

The Deployment Timeline Is the Pivot Point

The investment case for ASTS ultimately hinges on the satellite deployment schedule. The company’s goal of reaching 45 to 60 satellites in orbit by year-end 2026 is the key catalyst — because that’s the constellation size at which recurring commercial service revenue becomes meaningful.

The roadmap calls for launches roughly every one to two months on average through the rest of 2026. Analysts forecast ASTS losses of approximately $0.69 per share for 2026, narrowing to profitability in 2027, with EPS potentially reaching $7.00 in 2028. If that trajectory holds, the Palantir parallel becomes even more apt — a long wait, followed by a sharp inflection.

The Bottom Line

ASTS is unquestionably a “yeah, but” stock right now. Analysts are cautious, the stock is ahead of consensus, and profitability is still not on the near-term horizon. But the boxes the company is checking — record-setting satellite technology, $1.2 billion in contracted revenue commitments, 50+ mobile network operator partners representing nearly 3 billion subscribers globally, and a war chest of nearly $4 billion — are not small boxes.

Palantir’s story taught investors that the market sometimes prices in transformation before the income statement catches up. The question for ASTS shareholders is whether history is about to rhyme again. The unusually high institutional ownership, relative to Palantir at a comparable stage, suggests the smart money is already betting that it will.

Leave a Reply