CoreWeave (NASDAQ:CRWV) might provide ultra-aggressive speculators with an opportunity to scalp some quick profits, though it will practically be a binary affair. On Thursday after the market close, the artificial intelligence cloud-computing company will release its fourth-quarter earnings report. Unlike many of its tech peers, CRWV stock is up strongly this year, gaining almost 39%. Thoughts of an AI bubble just don’t seem to affect the graphics processing unit infrastructure specialist.

Table of Contents

Of course, we’ll find out just how much the market truly believes in CRWV stock. For Q4, Wall Street analysts anticipate a loss per share of 65 cents on revenue of $1.53 billion. In the prior sequential quarter, CoreWeave posted a loss per share of 8 cents on revenue of $1.36 billion, beating out the consensus targets of a 52-cent loss and $1.28 billion in sales, respectively.

To be quite blunt, talking about analysts’ expectations isn’t magically going to reveal insights. Just because the company is on a growth trek does not necessarily entitle us to believe that CoreWeave can deliver the goods. Even if it did, there’s really no telling how CRWV stock will react. Per philosopher David Hume, the future is not necessarily compelled by the past.

That said, how the options market is pricing risk could give us important clues as to what the smart money is most concerned about.

Volatility Skew Provides Key Intel for CRWV Stock

As I mentioned in multiple articles for StockEarnings.com, volatility skew represents a critical indicator for retail traders. Definitionally, the skew identifies implied volatility (IV) — or a stock’s potential range of motion — across the strike price spectrum of a given options chain. In other words, the skew is a screener that showcases the surface-area distortion of volatility space, allowing traders to understand how the smart money is positioned for risk.

Probably the best way to explain volatility skew is a team’s formation in soccer. Most of the time, you’ll see teams adopt some variant of the balanced 4-4-2. In other cases, aggressive teams will opt for the 3-4-3 formation, sacrificing defensive coverage for more offensive pressure. With CRWV stock, for the upcoming Feb. 27 expiration date, the formation is roughly equivalent to the 5-4-1 formation.

In this setup, the team is sacrificing a forward to gain an additional defender. When it comes to CRWV stock, the skew for both calls and puts are clearly elevated to the left boundaries (toward lower strikes). That’s a defensive posture, especially with the skew on the right side gradually fading, then flattening.

Basically, we’re looking at a framework where smart money traders are not aggressively seeking upside convexity in CRWV stock. At the same time, nobody appears panicked; otherwise, the security would have likely sold off in the open market. Broadly speaking, high-level investors want exposure to CoreWeave but they want to be smart about it.

However, every action has a reaction. If CRWV stock is in a defensive shell, for lack of a better phrase, then bullish expression through call options should be discounted. As such, if there’s a legitimate reason to buy CoreWeave, it could be an enticing opportunity.

Figuring Out a Game Plan for CoreWeave Stock

While we now understand the basic risk positioning of CoreWeave stock, we must figure out a mechanism of translating this information into tangible price outcomes. For that, we may turn to the Black-Scholes-derived expected move calculator. Wall Street’s standard mechanism for pricing options provides a dispersion between $84.06 and $114.32 for the Feb. 27 expiration date.

To be brutally honest, the expected move calculation is simultaneously useful and useless. Using the above soccer analogy, if the volatility skew is akin to a team’s formation, then the calculator is the available passing lanes for a player. Typically, someone with the ball may have two or three safe passes, including one going back to the keeper. There may also be a handful of highly dangerous but heavily contested passing lanes available.

Again, this info is both useful and useless. Soccer is a game that usually features multiple passes in an attempt to expose defensive mispositioning. Stated differently, games are often decided by the exploitation of structural weaknesses that flash dynamically rather than statistically. And it’s here where we arrive at a key problem with Black-Scholes.

If you look at the actual equation, it’s a static formula, with the only variable inputs being volatility. In other words, no matter what stock is plugged into the formula, the essential output — a perfectly symmetrical price dispersion — is identical; the only difference is that some securities are more volatile than others.

Where I have a fundamental disagreement with mainstream financial analysis is that I believe “scoring opportunities” are not static events waiting to be discovered, but rather fleeting windows of opportunity where market structure favors the speculator. We need a framework that studies this dynamism, which is where the Markov property comes into the picture.

Narrowing CoreWeave’s Probability Space

Derived from Russian mathematician Andrey Markov, the Markov property colloquially claims that the future state is solely dependent on the current state. What are the chances that the present run of play will lead to a goal? For example, if an attack finds defensive players out of position, the odds greatly increase as opposed to when defenders are stacked and well-prepared.

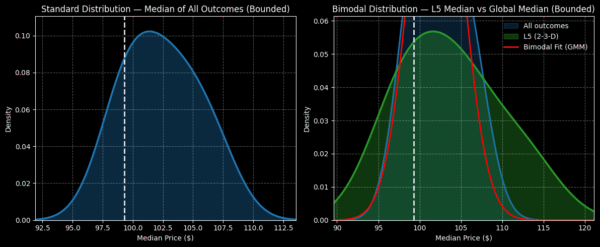

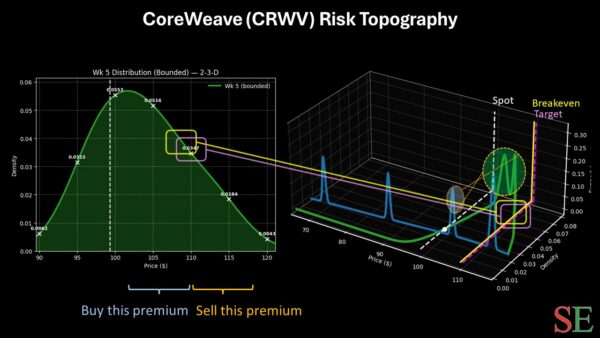

In the case of CoreWeave stock, in the last five weeks, CRWV printed two up weeks, leading to an overall downward slope. There’s nothing special about this 2-3-D sequence, per se. However, this quantitative signal represents a specific in-game situation — and that will likely have an influence on end results.

Using enumerative induction and Bayesian-inspired inference, we can estimate a forward five-week return landing between roughly $85 and $125. About 62.5% of the probability mass would be expected to fall north of the spot price, which statistically favors the bulls.

Considering that earnings reports tend to generate above-average volatility, I speculate that the above range may materialize post-earnings rather than over a five-week period. Plus, the range isn’t terribly far removed from what the Black-Scholes model is predicting, but with a more bullish bias.

Still, this is a risky concept. For the most aggressive, the 109/110 bull call spread expiring Feb. 27 could be interesting. For a net debit of $50, traders can potentially enjoy a maximum profit of $50, a 100% payout. CRWV stock will need to rise through the $100 strike by Friday’s end to make this trade happen. Breakeven lands at $109.50, presenting a very thin but cheap debit spread.

Leave a Reply