Kimberly-Clark Corp. (NYSE: KMB) stock is down after its earnings report on Jan. 27. The company was expected to give investors a snapshot of the consumer. It did just that, and the word for KMB stock, as well as many consumer staples stocks this earnings season, may once again be “value.”

Table of Contents

The company’s fourth-quarter 2025 report showed that its focus on delivering value applies to both consumers and shareholders. Kimberly-Clark emphasized its ongoing transformation, balancing cost controls, volume stabilization, and strategic growth bets – most notably its ongoing acquisition of Kenvue (NYSE: KVUE), the former consumer health division of Johnson & Johnson (NYSE: JNJ).

That acquisition, along with solid cash generation and a well-supported dividend, won’t make KMB stock a target of growth investors. But it strengthens the argument that value investors should be paying attention.

Meeting the Consumer Where They Are

“Acquiring Kenvue is a powerful next step in our transformation that will compound the momentum we’re already delivering across Kimberly-Clark. Importantly, it will also enable us to raise the standard of care for billions of people around the world,” said Kimberly-Clark Chairman and CEO Mike Hsu.

That strategic move comes as the company continues adjusting to shifting consumer spending. The fourth quarter reflected a stable-to-improving environment for essential product categories but continued sensitivity to price. Net sales came in at roughly $5.1 billion, up slightly from the prior year, with organic revenue growth of 1% driven by modest volume improvement and favorable product mix in tissues and personal care

Kimberly-Clark’s pricing discipline, cost productivity, and focus on “value-advantaged innovation” helped protect margins. Operating profit rose 5% year over year, aided by the ongoing implementation of its FORWARD program, which targets better supply chain productivity and marketing efficiency. While the consumer backdrop remains cautious, Kimberly-Clark’s ability to meet shoppers “where they are”—offering affordable essentials with strong brand loyalty—positions it well in a slow-growth economy.

Strength in Margins and Cash Flow

For a mature consumer staples name, margin expansion and consistent cash flow are the engines of long-term shareholder return. Kimberly-Clark delivered on both fronts in Q4. The company’s gross margin expanded by 60 basis points to 35.7%, reflecting moderating input costs, particularly in pulp and resins, and continuing synergies from manufacturing optimization.

Free cash flow totaled over $600 million in the quarter, supporting the board’s decision to raise the annual dividend to $5.12 per share. The current yield of about 5.0% is among the highest in the consumer goods sector and is consistent with the company’s long-term capital allocation framework.

Looking ahead, management guided to low single-digit organic sales growth in 2026 and mid-single-digit adjusted EPS growth on a constant-currency basis. That guidance leans conservative but reflects confidence that the business can maintain pricing power while balancing cost headwinds and global volatility. For dividend investors, the stability of those metrics underpins the company’s reputation as a “Dividend Aristocrat”—a company that has raised its payout annually for more than 50 years.

Challenges to the Thesis

Despite a solid operating foundation, KMB stock still faces notable headwinds. One is valuation relative to growth. Shares trade around 17 times forward earnings, a discount to peers like Procter & Gamble (NYSE: PG) or Colgate-Palmolive (NYSE: CL), but that discount is partly justified by KMB’s slower revenue trajectory. While organic volumes have stabilized, broad-based demand acceleration remains elusive, especially in developed markets where category saturation limits upside.

Inflationary and currency pressures also persist. Commodities may have moderated, but energy and packaging input costs remain volatile, and foreign exchange swings continue to trim reported revenue growth given Kimberly-Clark’s large international footprint.

Finally, the Kenvue integration—if completed as planned—brings both strategic potential and execution risk. Integrating overlapping product categories and navigating antitrust scrutiny could pressure near-term results. Investors will also be watching for updates on financing, as the company’s net debt position will likely rise to fund the acquisition, potentially constraining future share repurchases. While none of these issues derail the long-term value case, they suggest limited multiple expansion in the short run.

How to Play KMB Stock

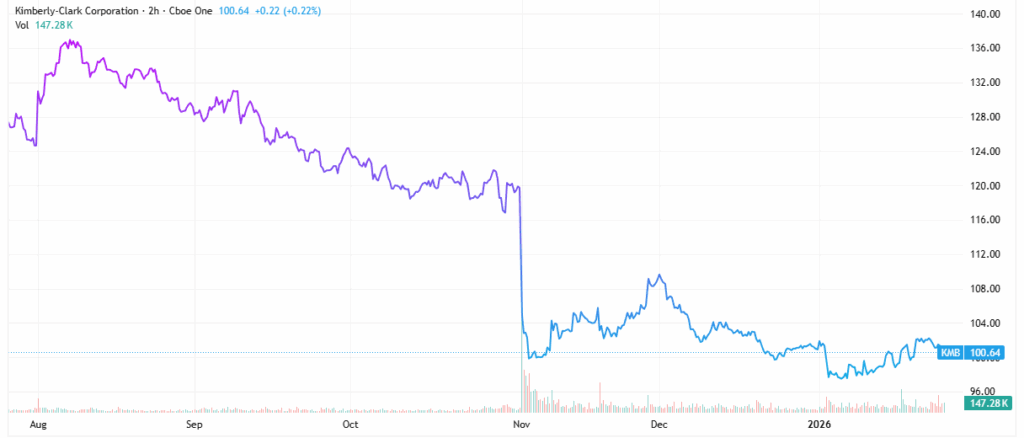

Using his proprietary quantitative model, Joshua Enomoto forecasted that KMB stock may be rangebound in an area between approximately $98 and $105. At the close of trading on the day of earnings, the stock is around $100, near the midpoint of that range.

That technical setup aligns with the broader consensus view. Wall Street analysts remain mildly bullish on KMB, with a consensus price target of $119, implying roughly 18% upside from current levels. When combined with a 5% dividend yield, the total return potential could reach the mid-teens annually, an attractive profile for investors seeking a lower-volatility equity anchor.

For tactical investors, KMB’s near-term trading range might favor “buying the dips” around $98–$99 to capture the dividend while waiting for potential re-rating catalysts such as synergy updates from Kenvue or better-than-expected volume growth in developing markets. From a portfolio construction standpoint, KMB can also serve as a defensive income play, balancing higher-beta holdings in technology or cyclicals.

The company’s disciplined capital allocation, proven pricing strategy, and focus on “value for consumers and shareholders alike” make KMB a steady compounder rather than a momentum name. That makes it appealing for long-term investors who prioritize stability, yield, and consistent capital returns over rapid capital appreciation.

Conclusion: Value in Stability

While Kimberly-Clark’s results didn’t ignite excitement in the broader market, they reinforced a dependable narrative: this is a company that delivers reliable returns even in uncertain times. Between its substantial dividend yield, improving margins, and the transformative Kenvue deal, KMB stock offers investors a mix of income and defensive resilience.

It’s unlikely to break out dramatically in the short term, but for those looking to anchor a portfolio with steady, inflation-beating cash flows, Kimberly-Clark may be one of the few true “value” names left in consumer staples.

Leave a Reply