Wayfair stock has been on a wild ride over the past year, and investors are asking whether this latest leg higher in W stock is the start of a sustained recovery or just another head fake. The online home-goods retailer has leaned hard into cost cuts and margin discipline after years of chasing growth at any price, and that shift is slowly showing up in its income statement even though earnings per share remain negative.

Table of Contents

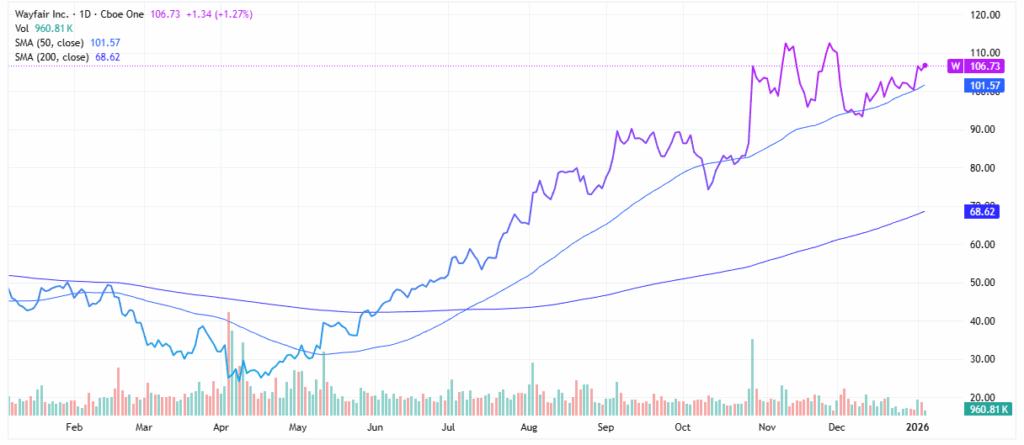

On the chart, Wayfair now trades well above its 200‑day moving average and is hovering around its 50‑day line, a spot where momentum traders often look to see whether buyers are still in control. For investors comfortable with volatility, Wayfair stock offers a high‑beta way to play a potential rebound in discretionary spending and e‑commerce, but the name still carries meaningful execution and macro risk.

A Tariff Reprieve is Spiking Wayfair Stock

Wayfair stock is up about 25% since its earnings report in November. That was due to the company beating on the top and bottom lines. The results were also higher on a year-over-year (YoY) basis.

That made sense because Wayfair caters to consumers who have been impacted the most by inflation. However, those gains were threatened by the Trump administration’s plans to raise tariffs on several furniture categories.

That’s no longer a concern since the administration has delayed the proposed increases until January 2026. That removes a significant potential headwind for Wayfair, which relies on global sourcing for many of its products.

Wayfair Fundamentals in Focus

From a fundamental standpoint, Wayfair remains a turnaround story rather than a mature, steady compounder. The company’s market cap sits around the mid‑teens in billions of dollars. Yet, as recently as the fourth quarter of its 2024 fiscal year, Wayfair was delivering negative earnings per share, which translates into a formally negative price‑to‑earnings ratio and reminds investors that true profitability is not yet locked in.

Management has emphasized expense discipline, logistics efficiencies, and rationalizing marketing spend to boost contribution margins, which is critical in a category where shipping bulky items can quickly erode gross profit. While revenue growth is likely to be tied to broader housing and consumer‑spending cycles, incremental improvements in operating leverage could have an outsized impact on future earnings power if Wayfair can sustain even modest top‑line growth.

Technical Setup for Wayfair Stock

Technically, Wayfair stock is trading in the upper portion of its 52‑week range, with the shares not far below their recent year high and well off the year low near the $20 level. The stock currently sits above both its 50‑day and 200‑day moving averages, a configuration technicians view as constructive because it signals an uptrend across multiple timeframes.

The 50‑day moving average is now well above the longer‑term 200‑day line, indicating the trend has already turned higher rather than just bouncing from oversold levels. For traders, pullbacks toward the 50‑day moving average may be seen as potential areas of support, while the recent year high represents an obvious resistance zone where prior buyers might look to take profits if momentum stalls.

Risk/Reward for Prospective Buyers

The risk/reward profile on Wayfair stock is nuanced and depends heavily on an investor’s time horizon and tolerance for swings. On the upside, if cost controls stick and demand stabilizes, the market could reward the company with a richer multiple as it moves closer to sustainable profitability, especially given how far the shares have rallied from their lows.

On the downside, Wayfair remains exposed to a soft housing market, weaker discretionary spending, and execution risk around logistics and customer acquisition, all of which could pressure margins and keep earnings in the red longer than bullish investors expect.

For now, Wayfair stock looks best suited for investors who can actively monitor the position, respect the technical levels on the chart, and size the trade appropriately within a diversified portfolio rather than treating it as a low‑volatility core holding.

Trade Ideas

For aggressive investors, the tariff delay plus improving execution supports a momentum‑plus‑fundamentals long in Wayfair, with any pullbacks toward recent support zones as potential add points while the uptrend remains intact. The 131% 12‑month rally and Mizuho’s 22% implied upside argue for scaling in rather than going all‑in at once, using position sizing and stop‑loss levels to manage volatility.

A tactical approach could be to trim partial profits into sharp spikes while keeping a core stake as long as tariff policy and margin trends stay favorable and the stock holds above key moving averages.

A Better Trade Than a Core Investment

Wayfair just picked up an unexpected tailwind: tariff hikes on key furniture categories are pushed out a year, easing a major macro overhang at the same time its marketplace model is proving it can handle pricing pressure better than smaller rivals. That combination of policy relief plus structural improvements helps explain why the stock has already more than doubled over the past year and still carries an additional upside case from Mizuho.

For investors, the opportunity looks attractive but not risk‑free, given ongoing exposure to discretionary spending, housing, and future trade decisions. In this phase of the turnaround, Wayfair fits best as a higher‑beta satellite position, sized carefully inside a diversified portfolio rather than a set‑and‑forget core holding.

Leave a Reply