The Hershey Company (NYSE: HSY) and Mondelez International (NASDAQ: MDLZ) are iconic names to many consumers. With Halloween in the rearview mirror and the holidays rapidly approaching, this should be a time for these sweet stocks to shine.

Both companies feature beloved, global snack and confectionery brands, have a history of innovation, and deliver consistent performance. All of which usually commands, or justifies, a premium valuation. However, this is an example of where a company and its stock are not the same thing.

It’s true that HSY and MDLZ are staples in many major exchange-traded funds (ETFs) that track U.S. consumer staples, dividend payers, and large-cap stocks. These companies provide stable, growing dividends and just enough growth to keep fund managers interested.

But here’s the catch. In a fund, these stocks probably carry very little weight. By contrast, as individual stocks in a retail investor’s portfolio, these sweet stocks have had a bitter history. And that underperformance could lead to a stomachache for investors at best, and a cavity in your portfolio at worst.

These Sweet Stocks are Testing the Patience of Long-Term Investors

Before we begin this analysis, let me be clear that I’m not suggesting that you should think of Hershey or Mondelez as a growth stock. But whether your goal is value or income, it’s important to understand that the two stocks have been laggards for some time.

Table of Contents

You can understand the problems over the last few years. These consumer staples giants have dealt first with a consumer wracked by inflation and higher borrowing costs that have eaten into disposable income.

The companies also face higher commodity prices, which make it difficult for them to provide competitive pricing to help the consumer.

You have to go back 15 years for HSY stock to deliver a total return of over 20%. It’s a similar situation with Mondelez. And that’s total return, which means it includes the company’s respective dividends, both of which have a yield of over 3%.

That means these two giant consumer staples stocks have underperformed the S&P 500 for some time. The question is why?

Margin Compression Continues to Pressure Earnings

Earnings (i.e., profits) are the single most important factor in stock price growth. Some may even call profits the mother’s milk of stocks. Over time, the best, long-term stocks are the ones that have a history of growing profits.

This isn’t to say that either company is on the verge of bankruptcy. These are both solidly profitable companies with many levers to pull to ensure they stay that way.

But investors look for margin growth, and both Hershey’s and Mondelez are reporting the opposite. In their most recent earnings reports, the headline numbers looked fine.

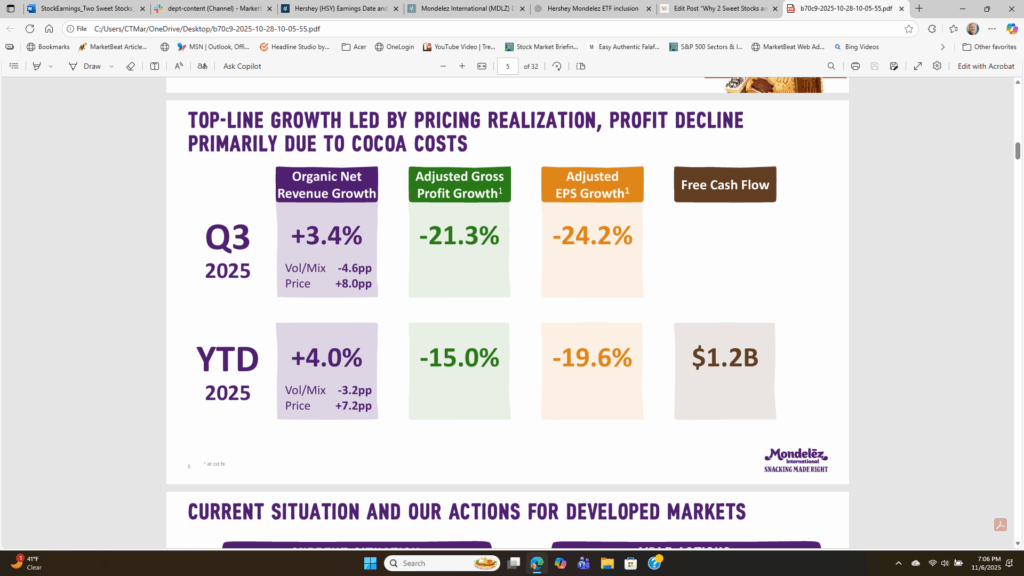

Hershey’s grew net sales by 6.5% in the quarter, and Mondelez churned out organic revenue growth of 3.4% for the same period. But the real story has to do with the impact of soaring cocoa prices, which have crushed each company’s margins.

Hershey’s gross margin plunged to 32.6% from 41.3% in the prior year, and its adjusted earnings per share (EPS) dropped by 44%. The story was no better for Mondelez. Its third-quarter gross margin was 26.8%, down from 32.6% year-over-year (YoY). The company also projected a double-digit decline in EPS for the full year 2025.

Here’s the kicker. This is happening even as the companies show ongoing top-line growth.

And margins aren’t expected to get better in 2026. Both companies believe commodity inflation will linger into 2026. There are only so many strategic initiatives and cost-cutting efforts the companies can make to dampen these headwinds.

Can Holiday Sales Make These Sweet Stocks Great Investments?

A common term you hear with consumer staples stocks is “pricing power.” This relates to a company’s ability to raise prices incrementally to offset margin concerns. Companies may also rely on volume leverage, meaning they simply sell more.

But Hershey and Mondelez are facing problems on both fronts. Each company has raised its prices but has found that price hikes have less impact when consumers are buying less of its products.

Hershey’s reported a 1% volume decline in its core confectionery unit that neutralized most of its 7% price increase. Mondelez reported a volume/mix slide of 4.6%.

Analysts cite the growth of GLP-1 drugs as a key culprit. For my money, I believe that Occam’s razor applies. Both companies rely on consumers who exist on the descending leg of our K-shaped economy.

Chocolate and other sweet snacks are enticing, but they are discretionary purchases. And when consumers are cutting back, those are luxuries that can go away. However, even if it’s cyclical and not systemic, it’s a problem that will take several quarters to solve.

The Bottom Line

I fear I’ve been too harsh on these companies. If you’re considering investing in either of these stocks, it’s essential to understand that they are solid businesses with loyal customers. Demand for these products will go beyond the upcoming holiday season.

But sweet stocks can still turn sour when market forces take over. And that means as much as you may love the products, there are better choices for investors in the short-term, even in the beleaguered consumer staples sector.

Leave a Reply